- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

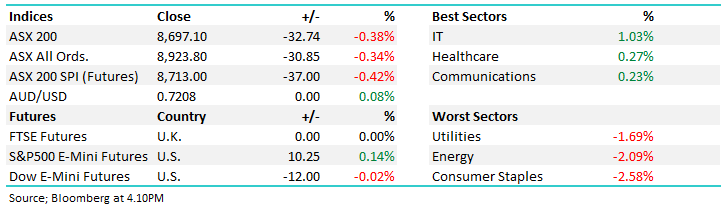

The ASX gave back some of Friday’s bounce today, drifting lower as softer local updates outweighed ongoing strength in US equities. Breadth was soft through the session with Staples and Financials leading the declines as the index whipsawed early in the session before cruising lower into the close. With the RBA decision due tomorrow and markets largely priced for another hike, investors remained cautious and selective.

- ASX 200: 8,697.10 / −32.74pts / −0.38%

- AUD/USD: 0.7208 / +0.08%

- Best sectors: IT +1.03%, Healthcare +0.27%, Communications +0.23%

- Worst sectors: Utilities −1.69%, Energy −2.09%, Consumer Staples −2.58%

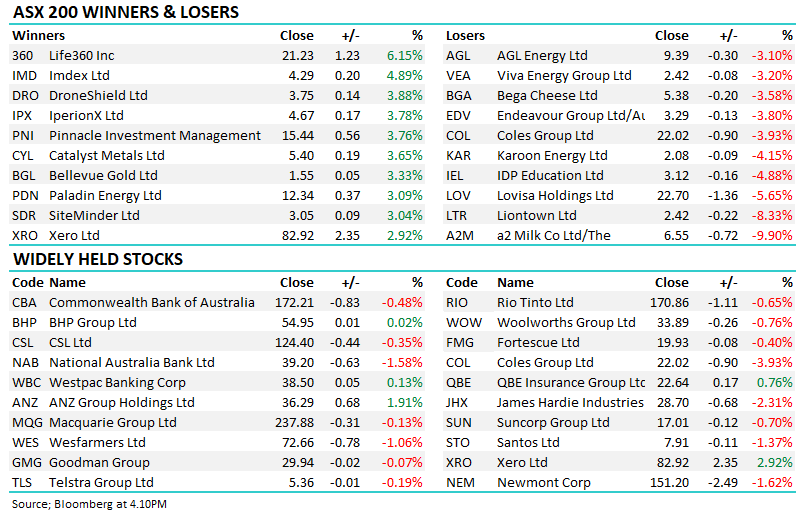

- Accent Group (ASX: AX1) −12.9% was hit hard, falling after downgrading 2H EBIT guidance by ~21% at the midpoint while also confirming it is assisting an ASIC investigation, adding another layer of uncertainty for investors.

- National Australia Bank (ASX: NAB) −1.58% weighed on the index after a slightly underwhelming first-half result, with margins and underlying revenue the key areas of concern despite headline numbers appearing close to expectations.

- The weaker tone across banks dragged Bank of Queensland (ASX: BOQ) −0.47% lower as well, with the sector continuing to grapple with margin pressure and rising costs.

- a2 Milk (ASX: A2M) −9.90% tumbled after launching a voluntary recall of US-labelled infant formula due to detection of a toxin, though the company noted no illnesses have been reported.

- Endeavour Group (ASX: EDV) −3.80% slipped following a softer-than-expected trading update, with management flagging subdued demand outside peak periods and rising input costs linked to fuel and freight.

- Woodside Energy (ASX: WDS) −3.05% and Santos (ASX: STO) −1.37% edged lower as crude prices eased slightly, though both remain supported by elevated oil prices in the context of ongoing Middle East tensions.

- Viva Energy (ASX: VEA) −3.20% was also softer, updating the market on its Geelong refinery restart timeline following last month’s fire, with production expected to return to above 90% capacity once repairs are complete.

- Navigator Global (ASX: NGI) went into a trading halt after announcing a $195m acquisition expected to be earnings accretive, funded via capital raise.

- GR Engineering (ASX: GNG) +1.09% secured a $57m operations and maintenance deal in the Beetaloo Basin over five years.

- Chrysos Corporation (ASX: C79) −4.49% fell after confirming FY26 guidance (rather than upgrading) as the market was positioned for.

- Nuix (ASX: NXL) −0.34% confirmed John Ruthven as permanent CEO after six months in the interim role

- Oil: trading around $US101.62/barrel (WTI) −0.4%

- Gold: trading around $US4,587/oz around our close. −0.6%

- Iron Ore: $108/mt / +0.4% for the day

- Asian Markets: China +0.11%, Hong Kong +1.58% and the Nikkei +0.38%.

- Global Futures: S&P 500 E-Mini +0.14%, Dow E-Mini −0.02%, FTSE 0.00%

- US Earnings Tonight: Palantir Technologies (PLTR US)