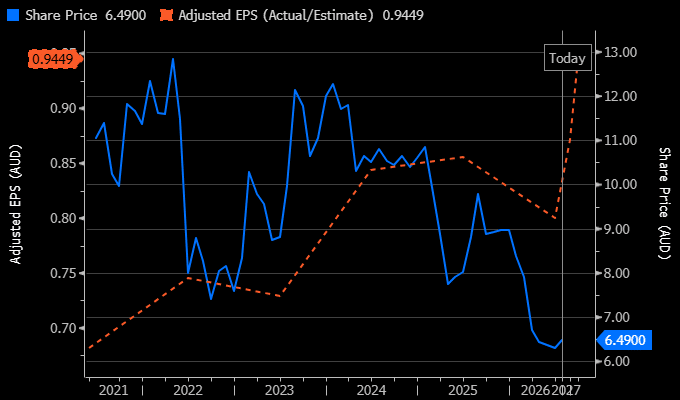

PEXA has been caught in the crossfire of regulatory headlines, after IPART flagged a tougher approach to regulating electronic lodgement network operator fees. That is clearly not ideal, and we do not want to dismiss the risk. PEXA’s Australian Exchange remains the profit engine of the business, and any move toward a more aggressive cost-based pricing framework could pressure returns. However, we think the market may be getting too focused on the regulatory overhang and not enough on the quality of the underlying asset.

PEXA operates the dominant digital property settlement platform in Australia, handling more than 80% of property transfers and around 90% of refinancing transactions. That is a very strong market position in a critical piece of financial infrastructure, and importantly, the recent ARNECC update was positive in that interoperability reforms will not proceed at this time. In simple terms, one of the bigger competitive threats has been pushed out, even if the trade-off is greater scrutiny on pricing.

The IPART review does create more uncertainty. IPART is looking at a building-block framework based on the efficient cost of providing electronic lodgement services, with the draft report due in June and a final decision expected by the end of September. The risk is that the regulator lands on a lower allowable asset base or return, which would reduce pricing and profitability in the Australian Exchange. This is certainly a real risk for PXA.

However, from our perspective, the current setup is not all bad. The decision not to proceed with interoperability removes a major structural risk, while PEXA’s core Australian platform still benefits from scale, entrenched industry usage and high transaction relevance. This is not a speculative technology business trying to prove product-market fit; it is already embedded in the property settlement system.

The other part of the story is the UK. PEXA International remains loss-making today, but it is also where the upside sits. They have had some good recent wins, including the launch of Tier 1 lender NatWest on PEXA’s platform for remortgages, with sale and purchase expected to follow by the end of CY26. If that traction encourages more major lenders onto the platform, the UK opportunity could become far more valuable than the market currently gives it credit for. In any case, we think the market is ascribing relatively little value to the UK opportunity, despite the potential for international breakeven over the medium term.

Financially, the business is moving in the right direction. On consensus forecasts, group revenue will grow from $408m in FY26 to $492m in FY28, while EBITDA rises from ~$140m to ~$180m over the same period. Margins are also expected to improve as the business scales. That operating leverage is important, particularly if the UK begins to contribute more meaningfully.

We own PEXA in the Emerging Companies Portfolio, and despite the recent pullback, we remain positive. The regulatory backdrop will likely keep the stock volatile over the next few months, particularly into the IPART draft report, but we think the broader investment case remains attractive. PEXA is a high-quality infrastructure-like technology platform with a dominant domestic position, a large offshore opportunity and meaningful operating leverage if execution continues to improve.

- Regulatory risk has clearly increased but so too has the opportunity to own a very good business following a pullback.

MM remains long & bullish PXA ~$12.20

Add To Hit List