For pure-play data centre companies, whose primary business is building, owning and leasing data centre infrastructure, the two US giants are:

Equinix (NASDAQ:EQIX) — the world’s largest colocation operator, running more than 250 data centres in 70 metro areas across 32 countries. It’s the global benchmark for the co-location model — essentially the same business NextDC runs, but at a planetary scale.

Digital Realty (NYSE:DLR) — operating more than 300 data centres, serving 5,000+ customers globally. They are more focused on wholesale leasing to large single tenants.

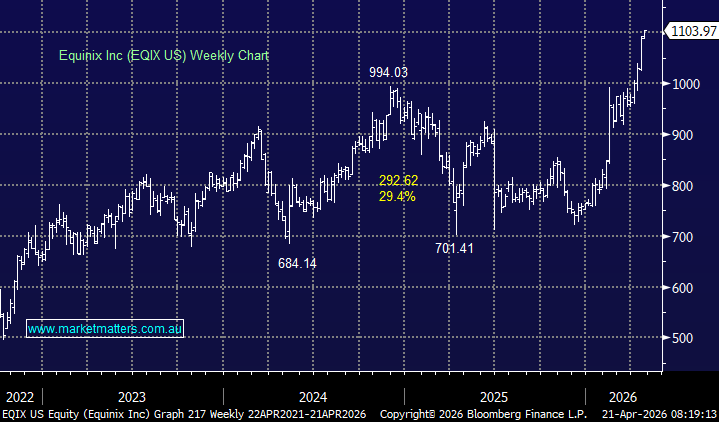

Equinix is the company NextDC most resembles, and probably most aspires to. Equinix has a market cap of roughly $US108 billion, compared to NXT, which sits at around $A9 billion. The gap illustrates both the scale of the opportunity and how early NextDC still is in its global journey. For investors trying to understand where NextDC’s ceiling might be, Equinix is the clearest reference point on the planet, assuming it can continue to expand its footprint across Asia.

Equinix’s move to new highs this month is a combination of broker enthusiasm, defensive rotation, earnings anticipation, and the broader re-rating of quality digital infrastructure assets. It’s a reminder of the valuation gap between a mature, profitable, dividend-paying global platform and an early-stage operator like NextDC still navigating its growth phase. The key difference being EQIX is now a defensive stock, a REIT paying a reliable dividend with recession-resistant recurring revenues.

- In line with our bullish outlook towards the US market through 2026, we believe the EQIX breakout will push higher.