- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

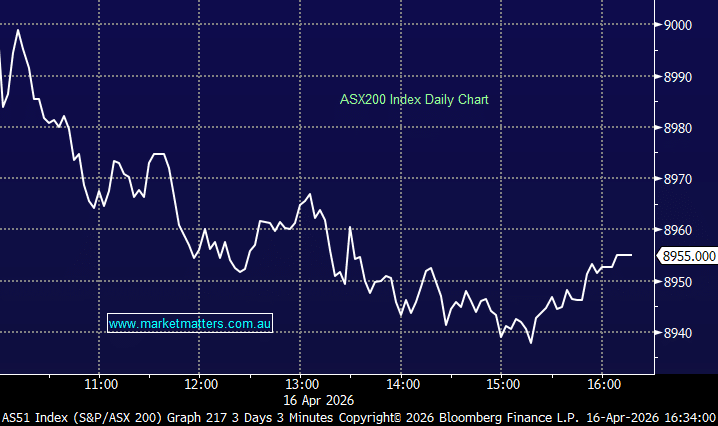

The ASX wavered today as investors balanced improving global risk sentiment against fresh domestic data. The local market initially opened higher following record closes on Wall Street, but struggled to hold early gains as traders digested Australia’s latest labour market report. Technology stocks lead the market again for the third straight day, with the sector +13.7% from the start of the week, albeit from a low base, as the rotation back into software names gathers momentum locally and abroad. The tech bounce meant little on the index level however, with heavyweight financials and materials dragging the overall bourse lower.

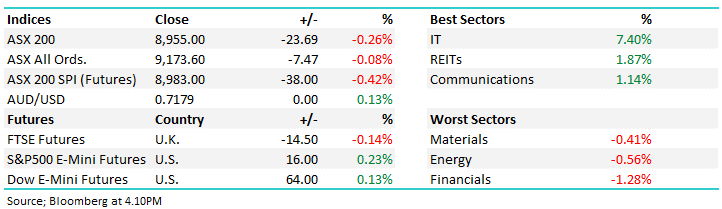

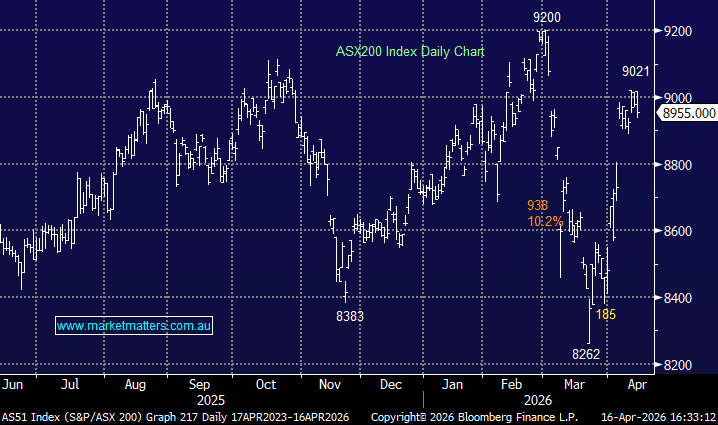

- ASX 200: 8,955.00 / −23.69pts / −0.26%

- AUD/USD: 0.7179 / flat / +0.13%

- Best sectors: IT +7.40%, REITs +1.87%, Communications +1.14%

- Worst sectors: Materials −0.41%, Energy −0.56%, Financials −1.28%

- Australia’s labour market remained resilient in March, with 17,900 jobs added while the unemployment rate held steady at 4.3%, broadly in line with expectations.

- Domestic conditions remain relatively tight despite the emerging global energy shock linked to the Iran conflict. Markets are now pricing roughly a two-thirds chance of another RBA rate hike in May, with expectations the cash rate could climb toward 4.6% by year-end.

- WiseTech Global (ASX: WTC) +12.36%, Xero (ASX: XRO) +9.00% and Life360 (ASX: 360) +12.45% all rallied sharply as investors extended the rebound across global software names.

- Real estate stocks also traded firmly with Goodman Group (ASX: GMG) +3.98% and Charter Hall (ASX: CHC) +1.75% gaining ground.

- Energy stocks were mixed — Ampol (ASX: ALD) +0.15% rallied after rival Viva Energy (ASX: VEA) was placed in a trading halt following a major fire at its Geelong refinery, potentially tightening domestic fuel supply in the near term. Meanwhile Woodside Energy (ASX: WDS) −1.06% and Santos (ASX: STO) −1.03% edged lower.

- Uranium names were stronger, with Paladin Energy (ASX: PDN) +2.61% and Deep Yellow (ASX: DYL) +2.27% both advancing as investors continued to favour nuclear as the preferred energy exposure moving forward.

- The materials sector weighed on the index – BHP Group (ASX: BHP) −0.34% and Rio Tinto (ASX: RIO) −0.70% both slipped, while large-cap gold miners were weaker with Evolution Mining (ASX: EVN) −4.15% and Newmont (ASX: NEM) −5.06% declining.

- ASX Ltd (ASX: ASX) +1.15% edged higher even after S&P Global Ratings downgraded the exchange operator’s credit rating from AA- to A+, citing governance and operational concerns flagged in ASIC’s review of clearing and settlement systems.

- Netwealth (ASX: NWL) +5.88% rallied after reporting $4bn in net inflows during the March quarter, lifting funds under administration to $125.8bn despite market volatility. Hub24 (ASX: HUB) +4.00% and Praemium (ASX: PPS) +2.88% also moved higher.

- AMP (ASX: AMP) +3.58% also reported platform flows, after reporting $1.1bn in inflows year-to-date, while deposits in its AMP Bank Go offering rose $632m in the first quarter of 2026.

- Ora Banda Mining (ASX: OBM) +10.27% jumped after reporting record quarterly production of 38,766 ounces, up 21%, generating $76.3m in free cash flow.

- Orica (ASX: ORI) −1.55% edged lower after warning supply disruptions linked to a third-party ammonia plant outage in Western Australia could impact production until mid-May.

- Oil: Traded modestly higher to $US90.55/barrel (WTI)

- Gold: Firmed $US33 to $US4,815/oz around our close.

- Iron Ore: Rose +1.8% to $103.80.

- Asian Markets: China +0.7%, Hong Kong +1.7% and the Nikkei +2.1%.

- Global Futures: S&P 500 E-Mini +0.23%, Dow E-Mini +0.13%, FTSE −0.14%

- US Earnings Tonight: Taiwan Semiconductor Manufacturing Company (TSM US) and Netflix (NFLX US) the main ones to watch.