- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

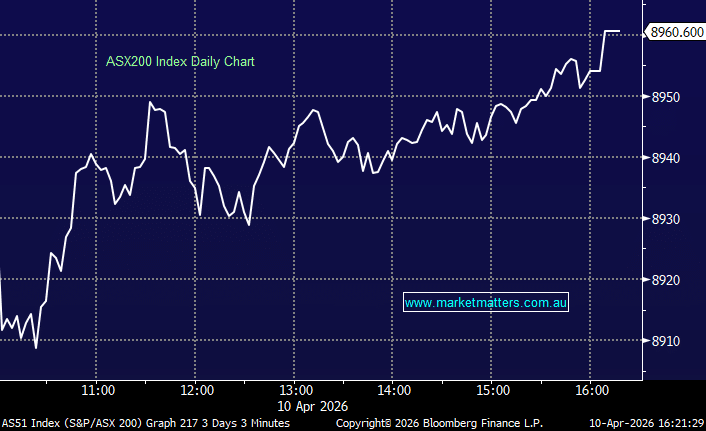

The local market softened today, though not by much, with the ASX200 still capping off a strong week, rising +3.3% over the period as markets continued to rebound following the US-Iran ceasefire. Risk appetite cooled with investors trimming positions ahead of talks between US and Iranian officials in Pakistan over the weekend, while uncertainty around the Strait of Hormuz and the resumption of tanker traffic continues to cloud the near-term outlook for energy markets.

Despite today’s softer finish, the tone through the week remained constructive with equities rallying strongly following the ceasefire announcement and oil prices heading for their largest weekly fall in more than nine months. Attention now turns squarely to US CPI tonight and the progress of ceasefire negotiations over the weekend, both of which are likely to shape sentiment for markets heading into next week.

- ASX 200: 8,960.60 / −12.61pts / −0.14%

- AUD/USD: 0.7064 / flat / −0.25%

- Best sectors: REITs +0.88%, Utilities +0.34%, Financials +0.32%

- Worst sectors: Energy −0.48%, Materials −0.67%, IT −1.84%

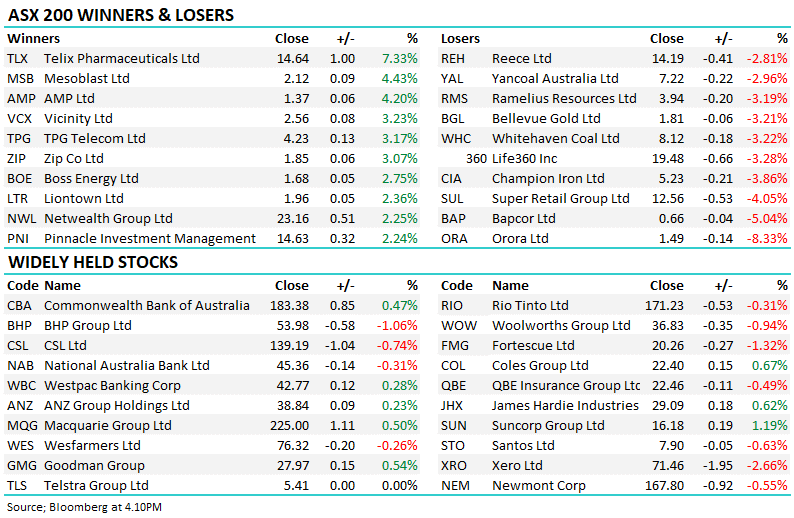

- Software and tech names were the weakest pocket of the market, tracking declines in US peers overnight — WiseTech Global (ASX: WTC) −2.56%, Xero (ASX: XRO) −2.66% and Life360 (ASX: 360) −3.28% all lost ground.

- Iron ore exposures were slightly softer – Fortescue (ASX: FMG) −1.32% slipped after outlining plans to accelerate the removal of fossil fuels across parts of its Pilbara operations, while BHP (ASX: BHP) −1.06% and Rio Tinto (ASX: RIO) −0.31% edged lower too.

- Energy producers were under pressure as easing geopolitical risk weighed on coal and oil sentiment – Whitehaven Coal (ASX: WHC) −3.22% and Yancoal (ASX: YAL) −2.96% led the sector lower, while Santos (ASX: STO) −0.63% and Woodside Energy (ASX: WDS) −0.15% also drifted despite Brent crude holding around the mid-high US$90s.

- Property names were a rare bright spot with Vicinity Centres (ASX: VCX) +3.23% leading gains across the REIT sector,

- Financials were slightly firmer with Westpac (ASX: WBC) +0.28%, ANZ (ASX: ANZ) +0.23% and CBA (ASX: CBA) +0.47% all edging higher, though NAB (ASX: NAB) −0.31% went the other way.

- Telix Pharmaceuticals (ASX: TLX) +7.33% jumped as US regulators accepted the resubmitted application for its brain cancer imaging product, marking another milestone in the approval process.

- AMP (ASX: AMP) +4.20% rallied after chief executive Blair Vernon said the group would prioritise growth in its wealth division, expand its use of artificial intelligence and tighten capital allocation.

- Magellan Financial (ASX: MFG) +1.18% edged higher after shareholders overwhelmingly approved its $1.6bn merger with investment bank Barrenjoey, with more than 92% voting in favour of the deal.

- Orora (ASX: ORA) −8.33% extended losses following the previous session’s sharp sell-off, with the stock falling again after an earnings downgrade tied to disruption at its Saverglass division and weaker demand linked to the Middle East conflict.

- Sequoia Financial (ASX: SEQ) −4.55% tumbled heavily after the corporate regulator launched court action related to the planned sale of its Interprac business.

- Oil: trading around $US98.50/barrel (WTI)

- Gold: trading around $US4,752/oz around our close.

- Iron Ore: Up +1% around $104.10/mt

- Asian Markets: All stronger China +0.7%, Hong Kong +0.7% and the Nikkei +1.2%%.

- Global Futures: S&P 500 E-Mini −0.06%, Dow E-Mini −0.14%, FTSE +0.12%