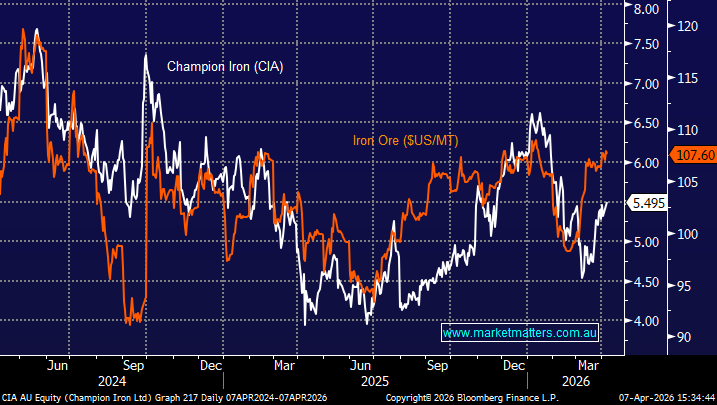

Champion Iron is a mid-cap iron ore producer focused on high-grade concentrate, with its core operations based in Canada’s Labrador Trough. To put things into perspective its iron ore revenue for FY25 was ~7% of BHPs before even considering copper, and coal. Apart from size, the key difference lies in costs, with BHP’s iron ore operations sitting structurally lower on the cost curve (~$US45–50/MT AISC) versus Champion (~$US65–70/MT), providing a clear margin advantage, particularly in softer pricing environments. In contrast, CIA relies more heavily on high-grade premiums to offset its higher cost base.

- Champion Iron is a pure-play, high-grade iron ore producer, offering leveraged exposure to iron ore prices with a structural advantage in premium product—but with more concentration risk than the diversified majors.

Champion Iron delivered an ok operational Q3 result in January with record sales (~3.9Mt), stable production (~3.7Mt) and improving costs, alongside strong profitability (EBITDA ~$150m, NPAT ~$65m). Cash costs continued to trend lower, and progress on the DRPF project reinforced the longer-term “green steel” growth story. However, the market was disappointed, with the stock falling ~4–5% on the day and continuing lower over the following weeks. The sell-off reflected softer-than-expected revenue, declining high-grade premiums and broader concerns around iron ore sentiment, highlighting that macro and pricing dynamics outweighed solid execution.

Champion Iron is progressing its DRPF project at Bloom Lake, with commissioning underway and first shipments expected by June 2026, while reducing site stockpiles and maintaining strong liquidity of around $750mn. The company is also expanding its high-grade footprint via the ~$US289m bid for Rana Gruber, alongside advancing the Kami project feasibility study with completion targeted by year-end. In February, Champion Iron raised $US100m via a private placement to La Caisse to help fund its Rana Gruber acquisition, with La Caisse increasing its stake to ~8.5% and existing shareholders diluted by ~5%.

- We can see CIA trading higher this year but will need to deliver operationally like its “big brothers”.

MM is cautiously bullish toward CIA around $5.50

Add To Hit List