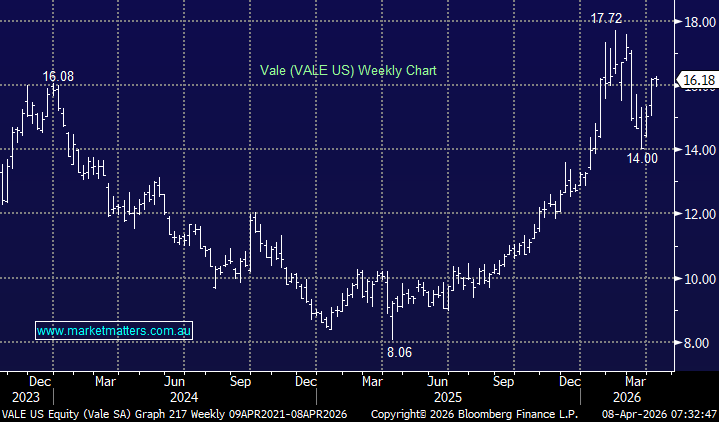

Vale is a US-listed, Brazil-based global mining giant and one of the world’s largest iron ore producers. A tier-one operator, it is increasingly diversifying into battery metals—primarily nickel and copper—which now account for more than 20% of group revenue. The stock has been outperforming the bulk commodity over the past nine months, with Citi recently lifting its price target by ~30% to $18, highlighting improving sentiment despite ongoing geopolitical risks.

Notably, Vale reports its production update on the 16th and 1Q earnings on the 28th, making this a key month for the stock.

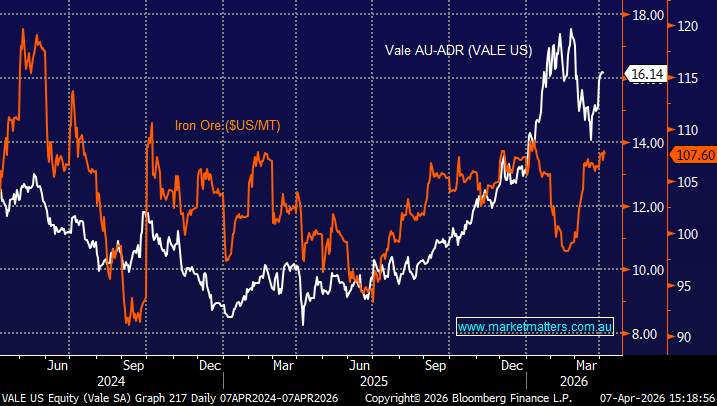

Strategically, Vale remains focused on organic growth, investing ~$US5–6bn in 2026 to optimise existing assets and enhance productivity, while targeting a doubling of copper output over the next decade. Like BHP and Rio, it is leaning into energy transition metals, while also pivoting toward India as a key source of future demand. With China’s steel demand plateauing, India is emerging as a critical growth market, with capacity expected to more than triple to ~500Mt by 2050.

- While India won’t replicate China’s scale, Vale expects to gain market share as this next leg of iron ore demand evolves.

Vale has followed a very similar path to BHP since “Liberation Day” and we expect that to continue targeting fresh highs from both mining goliaths this side of Christmas.

- We are targeting fresh highs above $US18 through 2026, or 10-15% higher.