We bought back into IREN overnight for the International Equities Portfolio, taking a small 3% position. While it’s not a cheap stock on current metrics, the investment case is now all about scale, execution and funding certainty as IREN accelerates its transition from Bitcoin miner to AI infrastructure owner – with earnings growth expected to be very strong in the coming years.

At its core, IREN is building large-scale, power-rich data centre infrastructure across North America, using a vertically integrated model that combines land, grid access and renewable-heavy power with compute capacity for both Bitcoin mining and AI cloud workloads. In a world where the constraint in AI keeps shifting from chips, to power, to labour, to deployment speed, IREN’s management argues the real bottleneck is now “time to compute” – in other words, how quickly capacity can be brought online. That plays directly to IREN’s strengths.

The latest numbers show the business is still in transition. In 2Q26, revenue fell to $184.7m from $240.3m in the 1Q, while adjusted EBITDA eased to $75.3m, reflecting weaker Bitcoin mining revenue as capacity is increasingly redirected toward higher-value AI workloads. On the surface, those numbers were softer, but beneath them the AI business is clearly becoming more important, and management now has the balance sheet and external funding support to keep pushing ahead.

Funding is crucial. IREN said in February it had secured $3.6bn of GPU financing for its Microsoft contract, with Microsoft prepayments and that financing together covering 95% of GPU-related capex. Cash and cash equivalents were $2.8bn at 31 January, while the company says it has secured more than $9.2bn of funding financial year-to-date across prepayments, convertible notes, GPU leasing and GPU financing. For a market that has often worried about how these fast-growing AI infrastructure stories fund themselves, that is a meaningful de-risking.

More recently, IREN announced it would expand AI cloud capacity to 150,000 GPUs, including purchase agreements for more than 50,000 NVIDIA B300 GPUs, with the enlarged fleet expected to support more than $3.7bn of annualised AI cloud run-rate revenue by the end of 2026. That’s a big ambition, and it is not fully contracted, but it shows the sheer size of the opportunity if the company continues to execute.

Our initial weighting reflects the risks. It remains a capital-intensive business operating in fast-moving end markets, and the stock will never be a low-volatility way to play AI. However, unlike last year when multiple expansion did much of the heavy lifting, the story today is increasingly backed by real capacity buildout, major counterparties, improving funding visibility and a scarce asset base in power-connected sites.

In other words, IREN sits at the intersection of two powerful thematics – digital asset infrastructure and AI compute, but it’s the second of those that matters most now. Daniel Roberts’ (CEO) recent comments that the industry is in “permanent whack-a-mole” mode ring true to us: every bottleneck that gets solved simply reveals the next one, and the winners are likely to be those with speed, access to power and proven delivery capability. IREN looks increasingly like one of them.

While not cheap today, from a forward valuation perspective, IREN is trading on 6.4x EV/EBITDA multiple for FY27, which is cheap given profits are expected to be 2.5x higher by then relative to FY25, and a market cap of about US$10.7bn. The analyst community is bullish, with 11 buys, 2 holds and 1 lone sell from JP Morgan. The consensus price target is $US81.23, nearly 100% above the prevailing price. In terms of the sell call from JP’s, they have a $US39 PT, which is around current prices, contrasting with Beirnstein (the most bullish) with a $US125 price target. Clearly some huge variance in assumptions, but the majority value it around ~$US80.

- This is a business that is evolving quickly, executing well, and importantly, has access to capital, land, power, and chips – all essential elements to meet the ongoing demand for data.

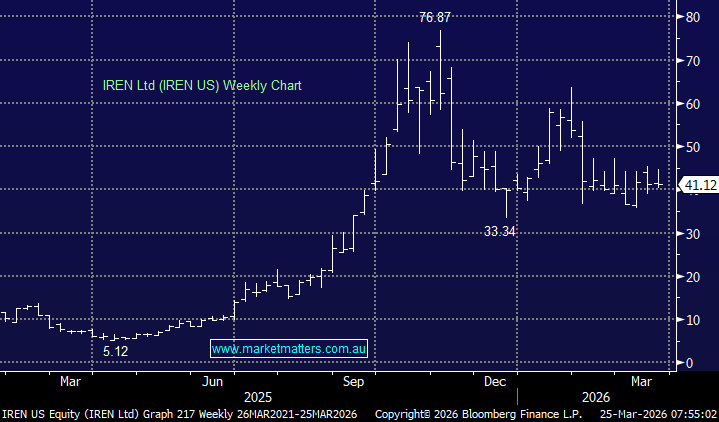

MM is bullish & now long IREN ~$US42

Add To Hit List