- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify

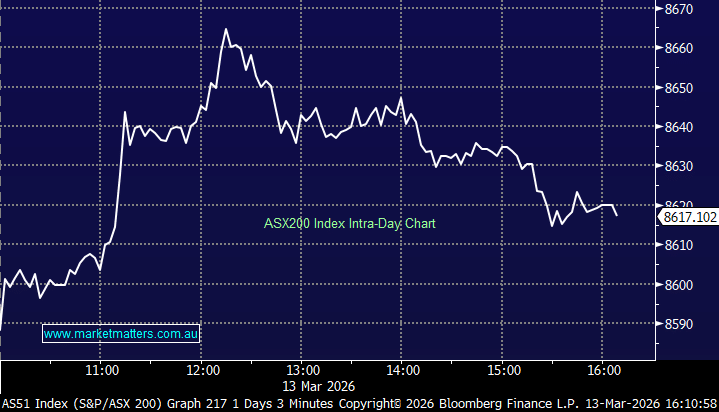

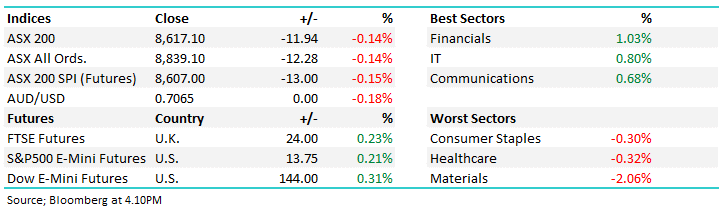

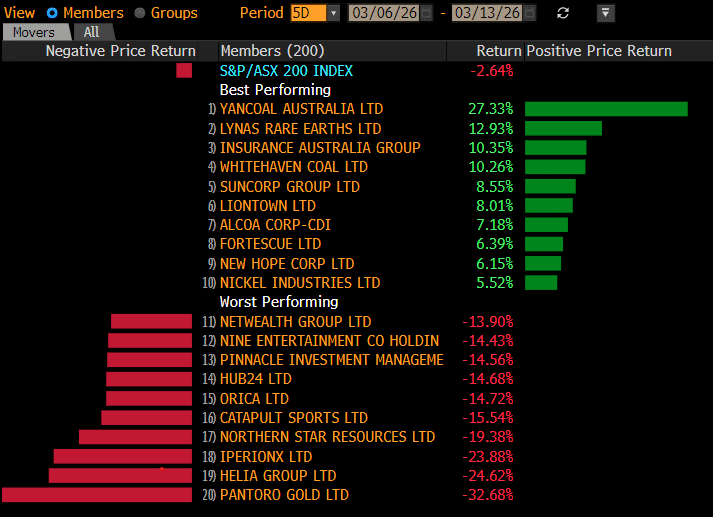

The ASX 200 ended Friday’s session down 0.14% at 8,617.10 — its lowest weekly finish since December, as a punishing week defined by Middle East tensions, RBA rate expectations, and a sharp rotation out of gold and materials weighed on the index. For the week the benchmark shed 2.6%.

The dominant forces were geopolitical and monetary policy related. The escalating Iran conflict drove oil above $US101/barrel, stoking inflation concerns and cementing market expectations of an RBA rate hike at Tuesday’s meeting – markets are pricing an 80% probability by close. That rate repricing drove a sharp rotation: banks were again the standout beneficiaries, with NAB leading at +1.5%, while gold miners came under significant pressure.

- ASX 200: 8,617.10 / −11.94pts / −0.14% (weekly: −2.6%)

- AUD/USD: 0.7065 / −0.18%

- Best sectors: Financials +1.03%, IT +0.80%, Communications +0.68%

- Worst sectors: Materials −2.06%, Healthcare −0.32%, Consumer Staples −0.30%

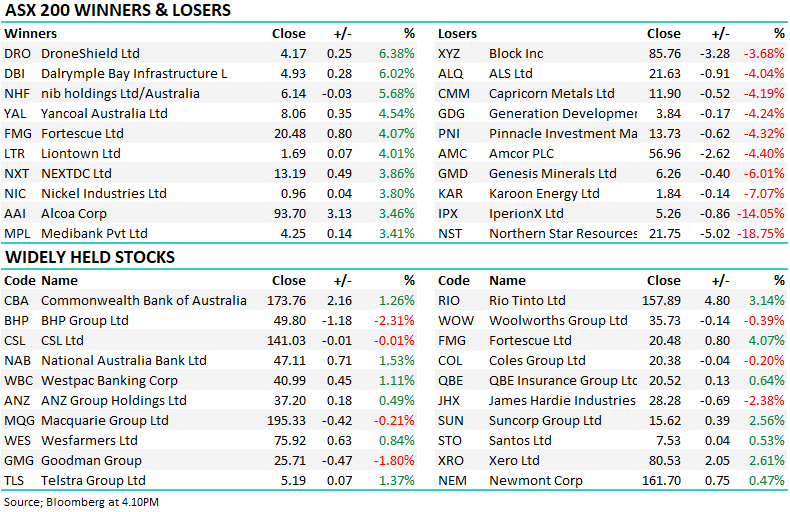

- Banks were the session’s clear winners as Tuesday’s rate rise was effectively priced in. NAB (NAB) +1.53% to $47.11 led the sector, with CBA (CBA) +1.26% to $173.76, WBC (WBC) +1.11% to $40.99 and ANZ (ANZ) +0.49% to $37.20 all firming. Net interest margin expansion remains the key earnings tailwind if the RBA moves as expected.

- DroneShield (DRO) was the ASX 200’s best performer, +6.38% to $4.17, after peer Electro Optic Systems (EOS) secured a $US42 million Middle East contract for its Slinger remote weapon system. EOS surged 16.9%.

- Dalrymple Bay Infrastructure (DBI) +6.02% to $4.93 after pricing its inaugural $350 million five-year fixed-rate bond at a 6.234% coupon, more than 2.5x oversubscribed — a strong result that reflects genuine investor appetite for quality infrastructure credit. There was also several broker upgrades through today on the stock

- Lifestyle Communities soared ~17% after US prefab giant Hometown America acquired 11.93 million shares at $4.90 via JPMorgan, with HMC Capital the seller. The land lease model continues to attract offshore capital.

- Fortescue (FMG) +4.07% to $20.48 — Macquarie flagged FMG as a direct beneficiary of China’s expanded ban on BHP iron ore, and the market agreed. A rare bright spot in an otherwise difficult session for materials.

- BHP (BHP) −2.31% to $49.80 as China widened its iron ore ban for a second consecutive week. The materials sector was the single biggest drag on the index.

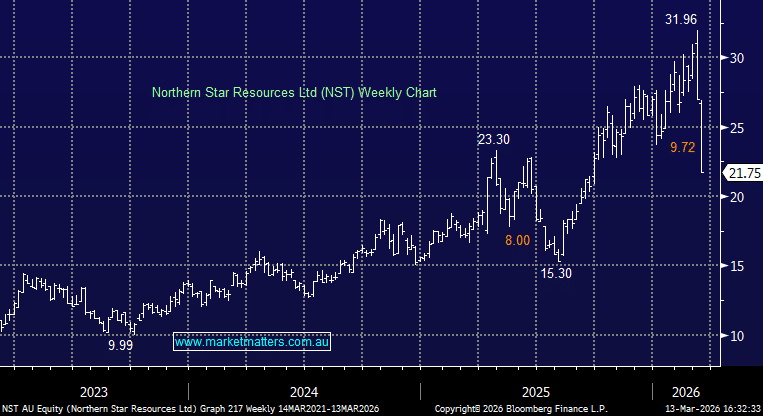

- Northern Star (NST) −18.75% to $21.75 was the session’s standout casualty. The company warned it would struggle to hit even the bottom end of its FY26 production guidance, citing weaker milling at the Kalgoorlie Super Pit and reduced output at Jundee. A significant miss versus expectations and a reminder that operational execution risk in gold mining is ever-present. Hard to step in front of this one until we see stabilisation.

- Immutep (IMM) plunged ~88% after its independent data monitoring committee recommended halting the Phase III TACTI-004 lung cancer trial following a negative interim analysis.

- Major shareholder Regal Partners (RPL) fell ~5.9% in sympathy. Not quite another Opthea moment but not a good look. Looks like they have around $75m in the stock.

- Syrah Resources (SYR) −28% fell after the US International Trade Commission rejected tariffs on Chinese graphite anode materials, removing a key near-term catalyst for the stock.

- Yancoal (YAL) +4.54% on the day and up ~19% for the week as Middle East gas supply disruption continues to drive energy-switching bets into thermal coal.

- Oil held around $US101/barrel despite the US temporarily relaxing restrictions on Russian supply. Iran maintained its pledge to keep the Strait of Hormuz effectively shut.

- Gold held above $US5,100/oz. Bitcoin near $US70,000.

- Asian markets: Hong Kong −0.3%, Japan -1.1%, China -0.2%

- US futures: S&P 500 E-Mini +0.21%, Dow E-Mini +0.31%, FTSE Futures +0.23%