- What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

The Afternoon Note failed to send yesterday– apologies. Here is the link to the note published on the website (logins not required).

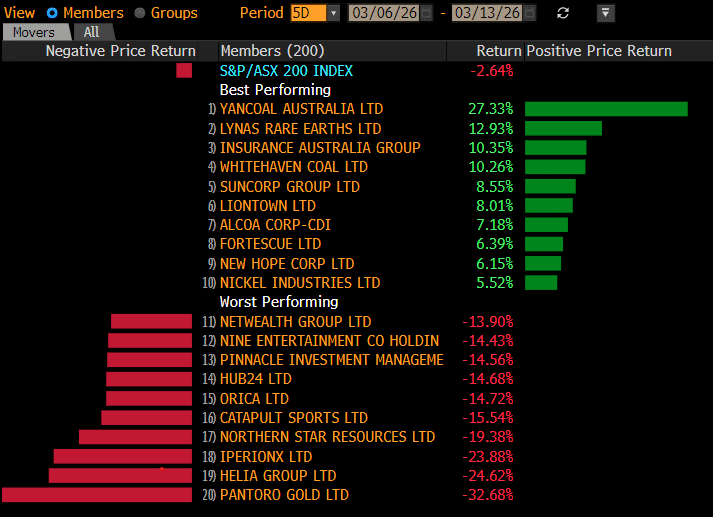

The ASX 200 endured another tough session on Thursday, falling -1.3% and chalking up another triple-digit decline. Several headwinds weighed on the market, most notably oil surging more than ~9% at one stage, with the knock-on impact on bond yields dominating the headlines. A plan by the International Energy Agency to release millions of barrels from strategic reserves failed to calm markets after reports that Iran struck oil tankers near the Strait of Hormuz, escalating fears of supply disruptions through the critical shipping route that carries roughly 20% of global oil trade. Every day Brent crude pushes above US$100 chips away at confidence that the global economy can quickly move past the Iran conflict.

- ANZ’s Commodity Strategist warned the oil market may be underestimating the risks to sustained supply losses, lifting the bank’s end-June Brent forecast to US$100/barrel.

Negative sentiment was compounded by an Iraqi official who told state media that oil ports “have completely stopped operations.” At this stage, it needs negative news flow to drive the oil price above the psychological level, but markets will rapidly start to lose patience with Trump & Co if the tide of this conflict doesn’t take a clear turn soon. In the last 24 hours, the surging oil price sent bonds tumbling, with the local 10s again flirting with the 5% level, ahead of next week’s RBA decision:

- Ironically, as Australian household spending fell for the first time since September 2024, the odds of a rate hike next Tuesday now sit at ~70%

Not surprisingly, the rate-sensitive tech and real estate sectors fared the worst on Thursday. At the same time, the materials weren’t far behind on fears of a global economic slowdown, with oil prices still feeling like a coil spring With it still trading above $US100 this morning, it’s likely to be a similar story on the performance front at the start of today’s session.

Overseas markets were weak overnight as a fresh surge in oil prices stoked fears that the war in Iran would further crimp energy supplies and fuel inflation, spurring another slide in stocks. In Europe, the French CAC fell by 0.7% while the UK FTSE closed 0.5% lower. In the US, the sell-off in US futures as oil prices rose continued with the Dow finishing down more than 700 points and the tech-based NASDAQ 1.7%.

- The SPI Futures are calling the ASX200 to open down ~30 points or 0.4% this morning following the weak session on Wall Street.