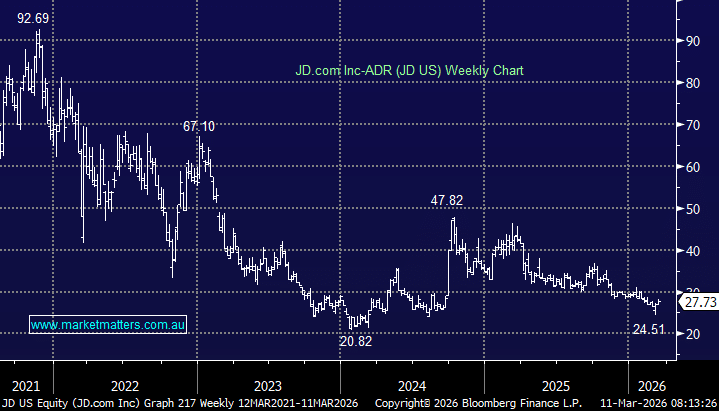

JD.com remains one of China’s key e-commerce players, combining a direct retail model with a third‑party marketplace and underpinned by a logistics network that continues to be a major competitive advantage. Alongside the core business, JD is building out several adjacencies, including JD Logistics, JD Health and JD Industrials, while also investing more heavily into on‑demand retail and food delivery. These newer areas are absorbing capital and weighing on near‑term earnings, but management is positioning them as longer-term growth engines.

Results out last week for Q4 were messy but overall, ahead of lowered expectations, which was enough to push the stock higher since.

- Group revenue rose 1.5% YoY to RMB352.3bn, a touch above consensus given the soft consumer backdrop.

- Adjusted EPS of RMB0.57 per ADR beat expectations, although JD still recorded its first quarterly net loss in almost four years, driven by heavy investment in food delivery and higher marketing spend.

- Margins bore the brunt of this step‑up in investment, with adjusted operating margin at –0.9% versus 3% a year ago.

- Adjusted EBITDA came in at a smaller-than-expected loss, while fulfilment costs increased 21% YoY.

Importantly, general merchandise sales grew around 12%, showing that JD’s core retail engine is holding up better than expected.

JD’s push into food delivery continues to be the main source of earnings pressure. Competition with Meituan and Ele.me has required substantial subsidies to attract users, driving rapid growth, reaching 240m users and around 15% market share since the 2025 launch, with a 30% share targeted over time.

Marketing costs surged as JD bought market share, tipping the group into a quarterly loss. Management suggested this investment cycle should ease in 2026 if competitive intensity doesn’t escalate further, which the market took favourably.

Outside food delivery, JD’s ecosystem is performing well:

- JD Logistics revenue up 22% with margin improvement

- JD Health revenue up 26%

- JD Industrials revenue up 17%

These divisions are becoming increasingly meaningful and help diversify JD’s revenue and earnings base. International expansion continues through JoyExpress and Joybuy.

While short-term profitability has taken a hit as they invest heavily in newer business lines, the core retail and logistics engine remains solid despite weak Chinese consumption. JD is still one of the highest‑quality operators in the space, backed by a logistics network that is extremely hard to replicate and a growing suite of adjacent businesses that broaden the profit pool.

- As food‑delivery investment normalises, we expect the market to refocus on JD’s underlying earnings power and the longer-term growth profile, supporting our positive view of the stock.

MM remains long & bullish JD US ~$US27

Add To Hit List