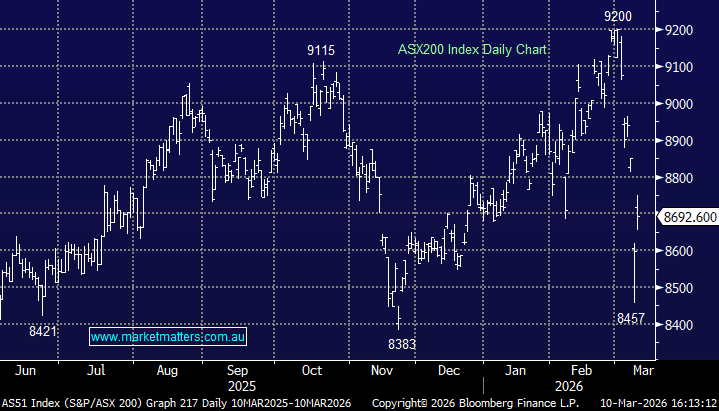

The ASX clawed back from Monday’s shellacking, closing up over 1% as Trump’s “pretty much complete” comments on the Iran conflict sent oil tumbling, giving markets room to breathe. It wasn’t a clean recovery. US futures are pointing modestly lower into the close and energy stocks copped heavy profit-taking as the oil tailwind reversed, but the bears didn’t get the follow-through they were looking for, and bargain hunters were active early.

The macro backdrop remains genuinely complex. Westpac consumer sentiment edged up 1.2% to 91.6 in March, but responses collected in the final three days of the survey, after the Iran escalation, implied a reading of just 84, the sharpest intra-survey deterioration in recent memory. Household spending for January came in at +0.3% m/m and +4.6% y/y, both below consensus, painting a picture of a consumer hugging the wall while rates stay elevated.

Bank of America broke ranks today, becoming the first major bank to call an RBA hike of 25bps at next week’s meeting, citing the oil shock as a “material” upside inflation risk. We’re not in that camp — we think the RBA should see April’s CPI print and the May 12 budget before moving. The data doesn’t force their hand yet.

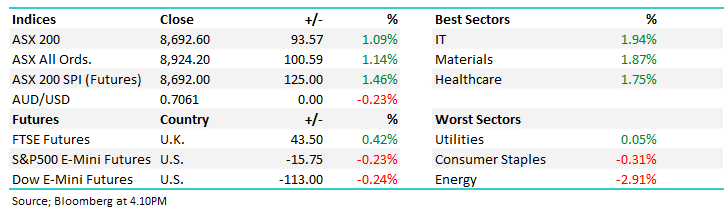

- ASX 200: 8,692.60 / +93.57pts / +1.09%

- AUD/USD: 0.7061 / down -0.2%

- Best sectors: IT +1.94%, Materials +1.87%, Healthcare +1.75%

- Worst sectors: Energy -2.91%, Consumer Staples -0.31%, Utilities +0.05%

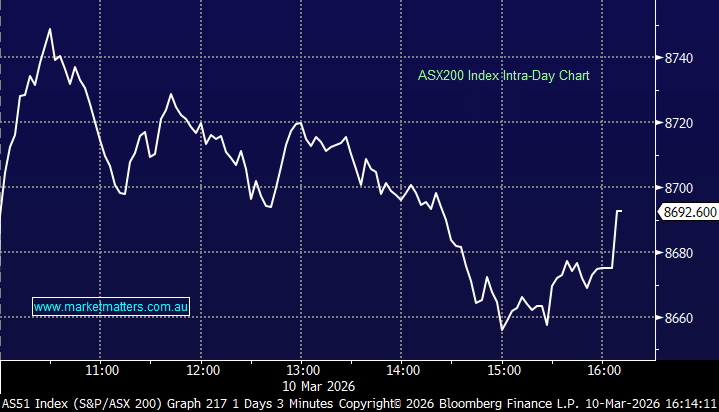

- The dominant theme remained the Iran war and its energy market implications, though today’s session saw a meaningful de-escalation trade. Oil fell ~25% relative to yesterday’s peak after Trump told CBS the military operation was “very complete, pretty much” and tracking well ahead of its initial four-to-five week schedule.

- At its peak on Monday, Brent had surged nearly 30% to just below $US120 — the largest single-session oil spike since the Gulf War era.

- The fall in Oil prices saw bond yields track lower – Aussie 3s down 8bps today at 4.47%

- That took some pressure off equities which bounced ~150pts this morning before finishing ~60pts below the morning highs – still some nervousness out there for sure.

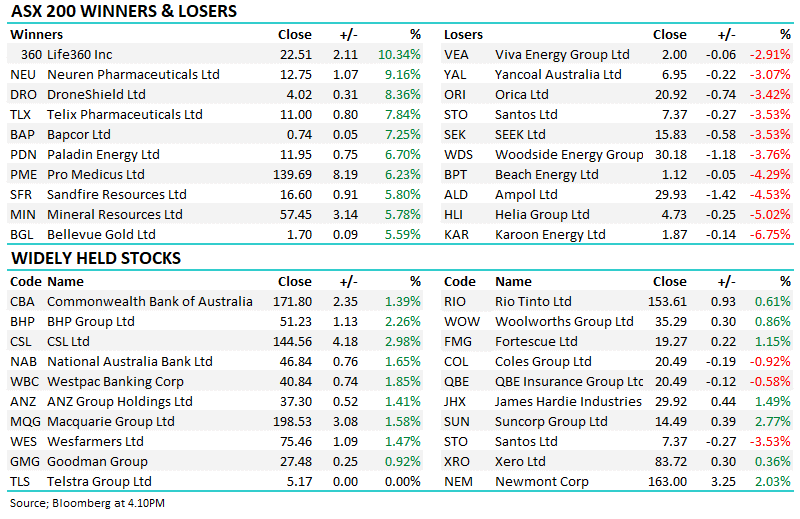

- Banks were a mixed bag after Wednesday’s heavy selling. ANZ Group (ANZ) +1.41%, Commonwealth Bank (CBA) +1.39%, Westpac Banking Corp (WBC) +1.85%, National Australia Bank (NAB) +1.65% and Macquarie Group (MQG) +1.58% all recovered ground, with Macquarie Group the standout in the sector after copping the heaviest selling earlier in the week.

- Suncorp (SUN) +2.77% bounced modestly today but remains near 52-week lows – we think a buying opportunity here

- WiseTech Global (WTC) +0.83%, Xero (XRO) +0.36% and TechnologyOne (TNE) +4.26% were all modestly higher, keying off a strong Nasdaq overnight. Life360 (360) was the standout of the day, up +10.34%.

- Woodside Energy (WDS) -3.76%, Santos (STO) -3.53% and Karoon Energy (KAR) -6.75% saw profit-taking as oil retreated — the reversal in energy names was sharp and consistent with traders unwinding Monday’s panic buying.

- Viva Energy (VEA) -2.91% and Ampol (ALD) -4.53% also gave back recent gains after China signalled refiners could resume some export activity.

- Golds bounced — Northern Star Resources (NST) +2.57% and Newmont Corporation (NEM) +2.03% both recovered modestly after Wednesday’s selling.

- GQG Partners (GQG) +0.53% had a relatively subdued day, but the thesis is building. GQG Partners attracted solid interest last week as investors started to appreciate that the fund manager’s defensive stance on technology could prove well-timed, with stronger near-term relative performance potentially driving renewed fund flows.

- New Hope (NHC) -2.70% gave back some of Wednesday’s Iran-driven gains as coal prices eased alongside oil on Trump’s de-escalation comments. Keep an eye on the 17 March earnings result — consensus EPS is around 8 cents for the half, and with coal prices still structurally elevated relative to pre-war levels, there’s a reasonable chance of a positive surprise.

- Property stocks were mixed – Mirvac (MGR) +1.6% was added to the Growth & Income Portfolios today – we see value in the sector, fading the move higher in bond yields

- Looking at the MM Portfolios: Growth was +1.1%, Income +0.65%, Emerging +1.6% & ETF +0.75%.

- International Equities Portfolio was +0.7% overnight

- Gold was trading +$US33/oz higher @ $US$5172/oz

- Oil was at US$88.50, down 6.6% on the session

- Asian Markets were up; Hong Kong +1.6%, Japan +2.95% and China +0.7%

- US Futures are down -0.25%