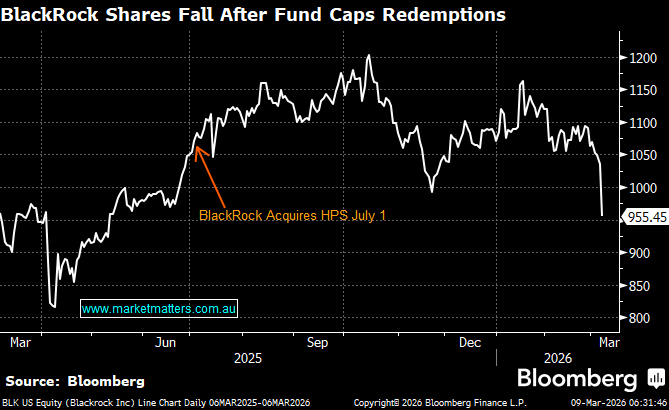

Private credit looked unstoppable when BlackRock paid $12bn for HPS Investment Partners, betting it could sell retail investors high returns from private lending. Just eight months later, cracks are appearing, with HPS forced to limit withdrawals from its $26bn flagship direct-lending fund after $1.2bn of redemption requests. The move has rattled confidence in the ~$3 trillion private credit market, raising concerns that lending standards weakened during the boom years and that retail investors may not fully appreciate the illiquid nature of these products. While most still see long-term growth, and we agree, the episode highlights early stress as the sector faces its first real test.

This fresh bout of concerns around private credit is currently taking second stage to the Iran conflict but in similar fashion it’s likely to throw up some great opportunities. The more concerns that wash through the global space the more quality managers will start trading at more compelling valuations – particularly for the large, high quality, diverse and very liquid global managers such as Blackstone (BX US) which we already own in the International Equities Portfolio and Blackrock (BLK US).