Last week was again volatile at the stock level as the local reporting season drew to a close, but the index forged ahead, absorbing what was thrown at it and closing up 1.3% at a new all-time high. The materials sector continued to do the heavy lifting, closing up +7.4%, ably supported by the consumer staples, which ended up 5%, while the retailers were a notable weak link with the consumer discretionary sector ending the week down 3.3%. With BHP surging more than $5, also closing at an all-time high on Friday, the market enjoyed a huge uplift from the “Big Australian” while beats trumped misses, which bodes well through 2026, although there were some standouts in both camps.

On the stock level, lithium stocks surged higher after Zimbabwe suspended exports, while the software names halted their slide as current earnings look good. As would be expected, a major portion of the noticeable “winners & losers” came courtesy of earnings season:

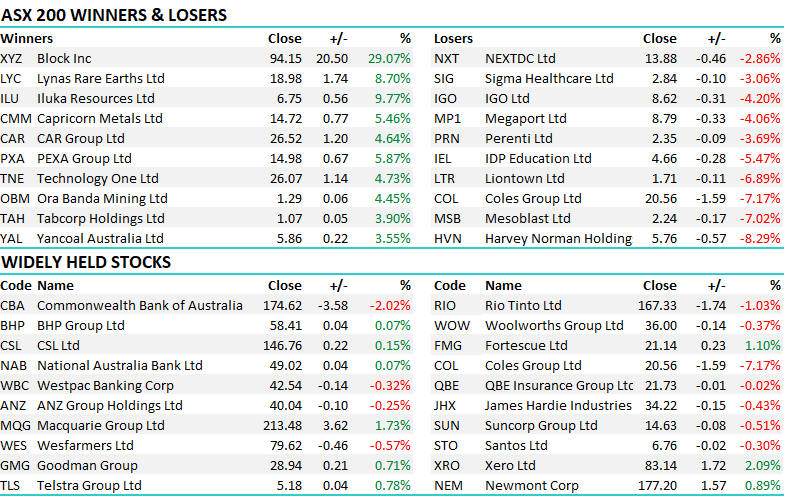

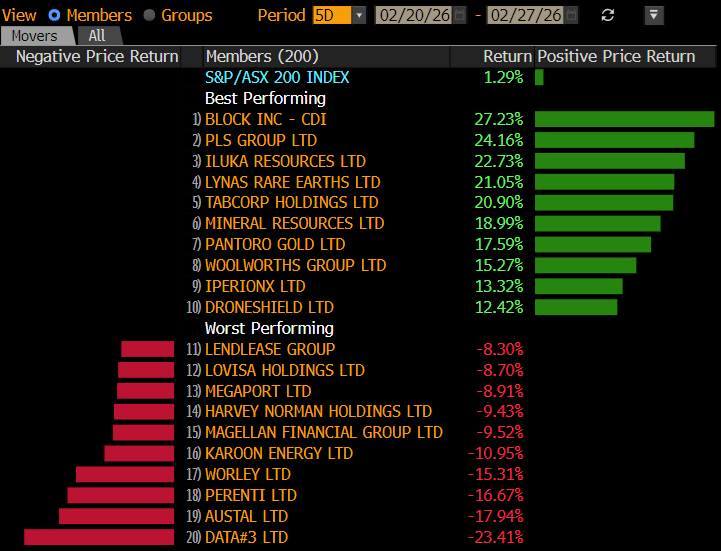

Winners: Block Inc (XYZ) +27.2%, PLS Group (PLS) +24.2%, Iluka Resources (ILU)+22.7%, Lynas (LYC) +21.1%, Pantoro Gold (PNR) +17.6%, Woolworths (WOW) +13.3%, Ramsay Healthcare (RHC) +11.5%, BHP Group (BHP) +9.5%, and Xero (XRO) +7.2%.

Losers: Data#3 (DTL) -23.4%, Austal (ASB) -17.9%, Perenti (PRN) -16.7%, Worley (WOR) -15.3%, Harvey Norman (HVN) -9.4%, Megaport (MP1) -8.9%, Lovisa (LOV) -8.7%, Web Travel (WEB) -8.2%, AGL Energy (AGL) -6.7%, and Qantas (QAN) -6.2%.

Weekly snapshot: The market-focused news was again all about reporting season last week, with concerns around private credit and risks around Iran weighing on US as opposed to local stocks:

- Markets started the week reacting to the US Supreme Court curbing President Trump’s tariff powers, prompting him to flag a temporary 15% blanket tariff on imports – investors simply bought defensives and sold software stocks.

- On Wednesday, the Australian CPI (inflation) print came in slightly hotter than expected, but stocks ignored the ramifications, roaring to new highs led by BHP, which surged over 3%.

- The collapse of Market Financial Solutions, a UK specialist lender providing bridging and buy-to-let property finance, saw aggressive selling in the US banks on Friday on private credit concerns.

- Friday’s sell-off in the US on credit concerns saw the S&P 500 endure its worst week since March, with sentiment not helped by a “hot” PPI, which reined in Fed rate cut hopes.

Overseas markets were mixed on Friday night, with bank shares under heavy pressure as the US KBW Bank Index fell as much as 6%, while private credit–linked stocks declined again amid concerns about potential fallout from the collapse of UK mortgage provider Market Financial Solutions. In Europe, the French CAC retreated -0.5% while the UK FTSE closed +0.6% higher. In the US, concerns around private credit created weakness in the banks, leading to the S&P 500 falling 0.4% and the Dow by over 500-points, or 1.1%.

- The SPI Futures are calling the ASX200 to open down -0.2% following Friday night’s weak session on Wall Street.