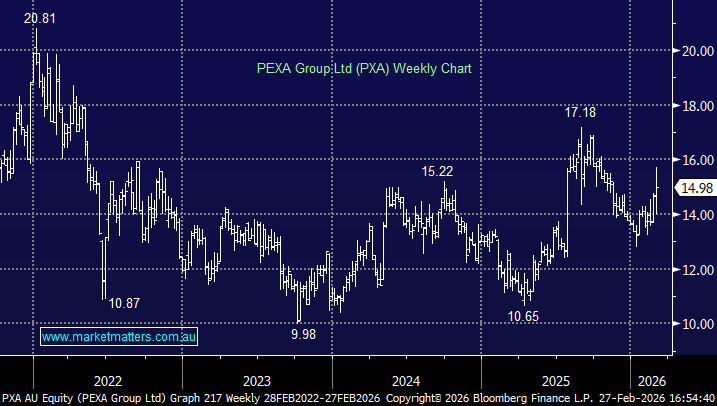

PXA +4.7%: PEXA Group rose as much as 9.9%, the most since July, after the Australian property exchange 1H EBITDA beat analyst expectations.

1H26 Highlights

- Revenue of $215.3mn, +9.9% YoY.

- Net loss of $14.3mn, v $32.7mn loss YoY.

- Group EBITDA from continuing operations of $85.8mn up 19% YoY.

- EBITDA margin increased 3.1% to 39.9%.

- Free cash flow increased 25% to $40.2mn.

- No dividend was declared.

This was a robust 1H result from the digital infrastructure business driven by record Australian transaction volumes, including a peak of 41,000 daily settlements in December 2025. Cost optimisation initiatives reduced local expenses by 2.6% and are expected to generate more than $10 million in annual savings. In the UK, volumes continued to recover, with sale and purchase transactions up 15% and remortgages rising 24%, alongside progress onboarding major lender NatWest and expanding services to conveyancers. The group also strengthened its balance sheet, repaying $25 million in debt as part of a broader capital management focus.

MM is long and bullish PEXA Group (PXA) around $15

Add To Hit List