Judo delivered a solid 1H26 result yesterday, with profit up strongly, loan growth tracking well and margins holding firm. Importantly, management reiterated full-year profit guidance, reinforcing confidence in the bank’s earnings trajectory as it continues to scale its SME franchise.

1H26 Highlights:

- Net income A$59.9m, up +32% half-on-half, reflecting continued operating leverage.

- Net interest margin 3.03%, stable and supportive of profitability despite a competitive lending environment.

- Gross loans $13.4bn, up +15% YoY, highlighting ongoing demand from SME customers.

- CET1 ratio 12.6%, down modestly from 13.1% as capital is deployed to support growth.

- FY gross loans guidance narrowed to $14.4–14.7bn, while pretax profit guidance held at $180–190m.

They highlighted that business credit demand remains solid, with growth running around ~9%, although cost-of-living pressures and global uncertainty remain areas to watch. Encouragingly, Judo continues to prioritise growth over dividends, reinvesting capital to expand its loan book, underpinning ~50% earnings growth in FY26, and ~34% in FY27 based on current consensus forecast, all while trading on 17x Est FY26 earnings.

Yesterday’s update reinforces JDO’s position as a high-quality niche SME lender, combining a strong margin structure with steady credit demand. While the modest narrowing of loan growth guidance is not significant, the decision to hold profit guidance steady speaks to confidence in margins and credit quality.

We like Judo’s differentiated model, targeted growth strategy and increasing scale benefits. Following the update, JDO remains firmly on MM’s radar for inclusion in the Emerging Companies Portfolio, particularly relevant for investors seeking exposure to domestic credit growth outside the major banks.

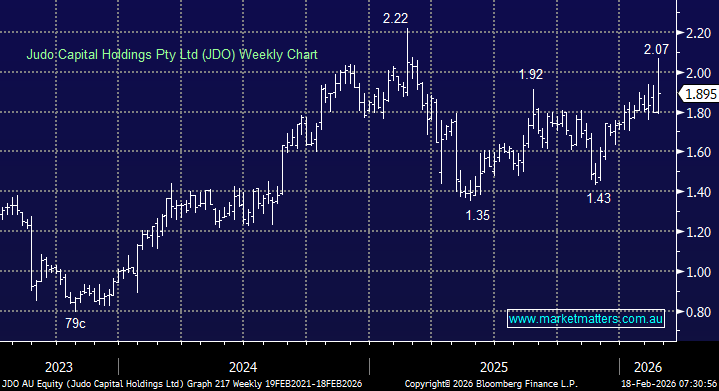

MM is bullish JDO ~$1.90

Add To Hit List