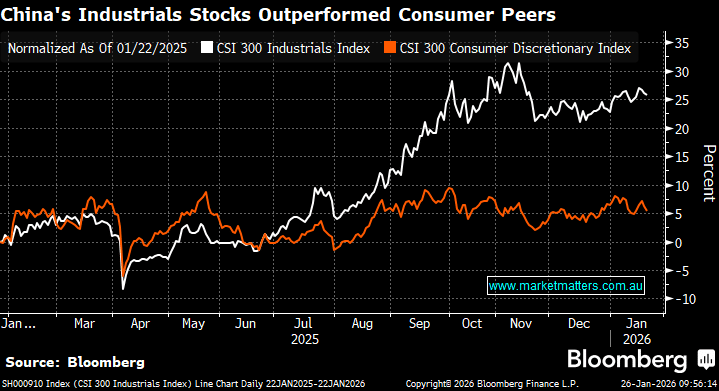

China’s equity market is increasingly split between two economies, with investors favouring export-focused industrial and technology winners over consumer-facing laggards. Manufacturing, equipment makers and metal producers are thriving on global demand for AI infrastructure, helping exports remain resilient despite tariffs, while domestic consumption continues to struggle under the weight of a painful property downturn. Their market mirrors the polarisation across the ASX, where miners are surging as growth stocks lag, reinforcing the case for active sector investing as we head into 2026.

However, with Beijing flagging reviving consumption as its top policy task this year, the sector’s valuations now look very attractive with policy support highly likely. At this stage, earnings forecasts for the CSI 300 Industrials Index have climbed 10% over the past six months, compared with just a 5% increase for its consumer peer – some catch-up by consumer facing stocks is our preferred path here, which would be supportive of companies like JD.com (JD US) and Alibaba (BABA US) which are both held in the International Equities Portfolio.

- We believe a more balanced approach across China’s market is now looking appropriate.