Citigroup has a chequered past with several operational missteps keeping them at the lower end of US bank rankings, generally trading at a large discount to their peers. Currently on a PE of 10.7x which is 16% below the sector average, Citi is undergoing a major turnaround under CEO Jane Fraser which includes a change in how each business unit operates and reports which should ultimately lead to better operational and financial outcomes.

- Investment banking is an important division, and they’ve just produced a very strong 4th quarter, which helped the group beat expectations with Fraser saying on the earnings call that market share had increased in all three main areas: advisory, debt and equity capital markets.

- In markets, they had the best Q4 in a decade; They’re huge in Fixed Income and revenue there was up 37% to $3.5bn topping both GS and JP Morgan while the much smaller equities unit also beat its bigger rivals with a 34% rise in revenue.

These trends are positive but there is a bigger focus for the CEO, improving returns. Citi remains at the low end of Wall Street for returns or in other words, it costs them too much to do business. Fraser has pushed through a massive reorganisation of the group over the past year, stripping out layers of management, selling off unwanted businesses and simplifying the organisation and we expect this to translate into higher returns over time, which should drive a re-rating of Citi’s multiple back towards the sector average.

This makes Citi our preferred Wall Street banking stock, with a combination of external tailwinds amplified by an operational improvement program that is starting to yield results.

- We like Citi and are adding it to the Hitlist for our International Equities Portfolio

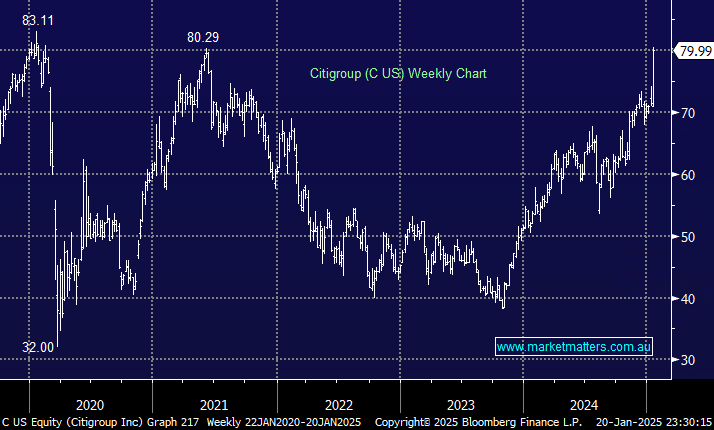

MM is bullish about Citigroup into 2025

Add To Hit List