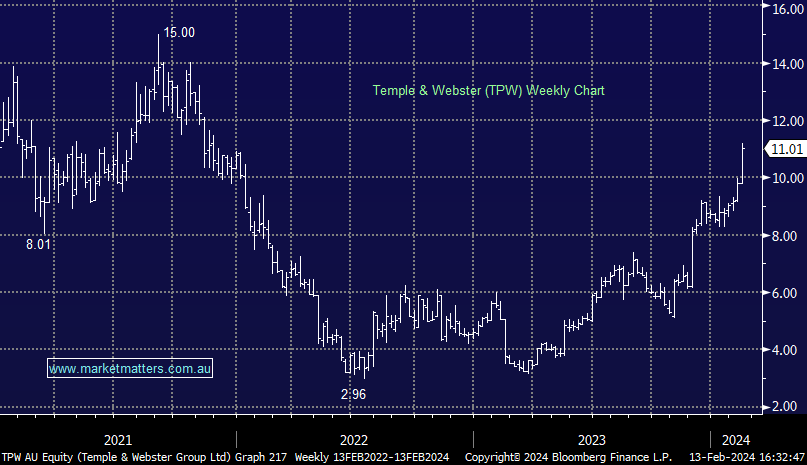

TPW +9.88%: two-year highs for shares in the furniture ecommerce business, and well deserved after a good 1H result. Revenue of $253.8m was only marginally ahead of the $251.4m expected, however, earnings were far better than the street, with EBITDA of $7.5m representing a 23% beat. The result came down to strong margins as costs continue to moderate with today’s result now showing a path towards longer-term targets of EBITDA margins around 15%. Trade in 2024 has also been strong with sales up 35% in the weeks to Feb 11th vs consensus looking for ~21.5% growth in the second half.

- A standout result as they inch towards lofty targets around earnings that the market has previously been skeptical on.

MM is neutral to bullish TPW

Add To Hit List