What Matters Today in Markets: Listen here each morning or find all Market Matters Podcasts on Spotify.

Global equities edged higher last week, with the US largely closed for business from Wednesday due to the Thanksgiving Holiday on Thursday, a far bigger affair to Americans than Christmas is to most Australians. The surge higher by stocks this month has caught many investors off-guard with the ~13% melt-up by US “Big Tech”, leading to inflows to global stock funds of about $US40bn in the fortnight through November 21st, although cash funds remain the clear winner year-to-date:

- Cash funds have received inflows of $1.2 trillion in 2023 compared to equities with $143bn, with a significant portion of the latter over the last few weeks.

The S&P500 is up +8.7% in November, one of its best performances in the last century, with December still to come. Assuming central banks, particularly the Fed, keep off their hawkish Tannoy’s into the New Year, we anticipate a pop to fresh 2023 and potentially new all-time highs in the coming weeks – only 1.3% & 5.7% higher, respectively. Investors are starting to believe that strong businesses are adapting well to higher rates, hence the strong getting stronger & vice-versa. However, as we move into Christmas, our preferred scenario is to see some performance reversion of the last 10 months as the headwind from soaring bond yields diminishes, and investors become comfortable that we’ve reached peak rates.

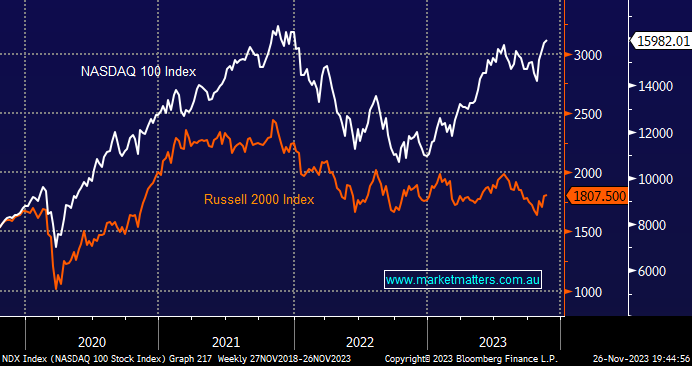

- We can see the Russell 2000 (small cap) Index outperforming the tech-based NASDAQ 100 into 2024, i.e. a “Risk On” environment.