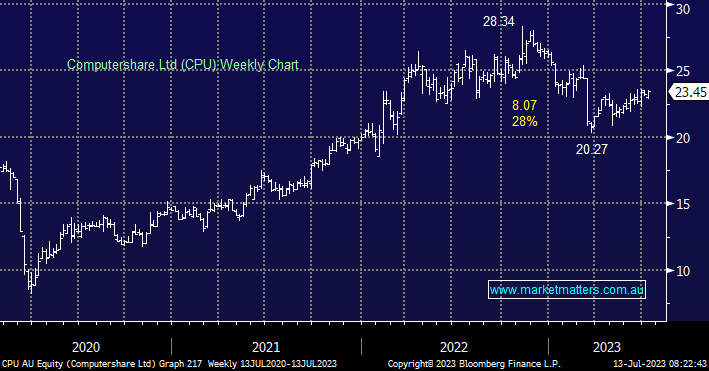

CPU provided a trading update in May with FY23 EPS growth of +90% reaffirmed but FY24 margin income guidance was reduced with lower average balances. At MM we’re still not huge fans of the registry and corporate services business especially with CPU being a beneficiary of higher interest rates this tailwind has come to an end in our opinion.

- We see no compelling reason to consider CPU around the $23.50 area.

MM is neutral on CPU

Add To Hit List