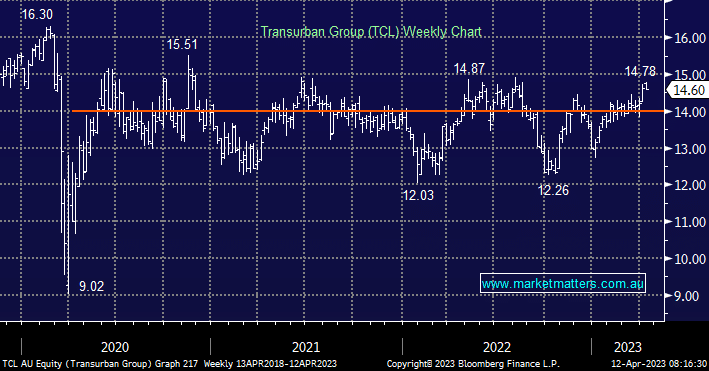

Yesterday, we took profits in toll road operator Transurban (TCL) at $14.68 having bought the stock back in April 2020 at $11.82. This has been a 3-year hold for a return of ~33% inclusive of dividends. While we like the company and believe that critical infrastructure has a place in portfolios, particularly those with a more defensive/income focus, valuation & opportunities elsewhere prompted the sale. In terms of valuation, like other infrastructure companies, we value fairly simplistically based on its yield above Australian 10-year bonds, which over the last 10 years has averaged 2%. Right now 10-year Treasuries sit at 3.22% while the consensus yield forecast for TCL over the coming 12 months sits at 3.90%, a spread of ~0.70%, a historically low margin. While earnings and thus dividends will grow over time, on FY24 forecasts the spread only jumps to ~1% then 1.32% by FY25. With ~90% of its revenues and earnings in Australia, (with the balance in North America), traffic flows here are very important, and while it’s recovered to pre-COVID levels overall, there is a greater number of heavy vehicles versus passenger vehicles making up the volumes implying that the work-from-home trend has further to play out, and ultimately we think the recovery in volumes post-COVID has now largely been achieved.

MM has now moved to a neutral stance on TCL, having sold the position from the Income Portfolio

Add To Hit List