TCL would be appealing to longer-term investors such as super funds who have been active in the M&A space over recent years, the company’s assets will continue to deliver while Australians drive cars plus its tolls are linked to inflation i.e. the gorilla in the room at present.

- We like TCL because it’s a quality business that could be in the crosshairs of global infrastructure investors, including our own super funds. NB: We hold TCL in our MM Active Income Portfolio.

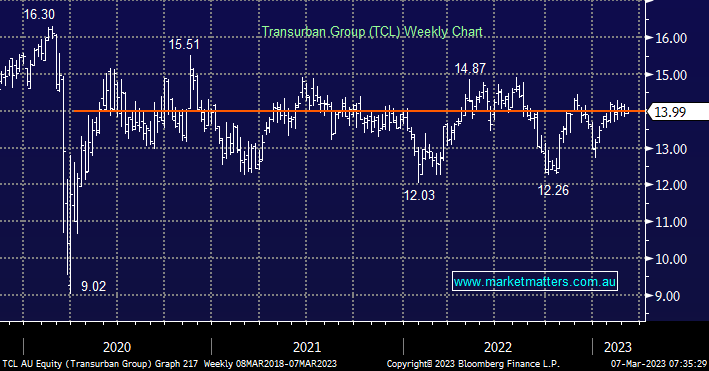

MM remains long and bullish TCL

Add To Hit List