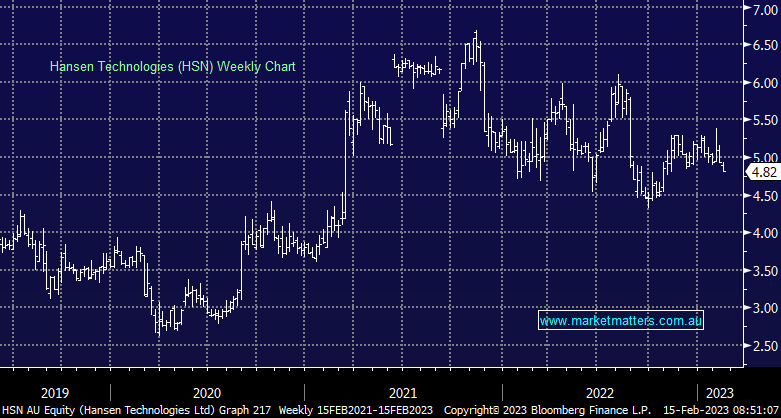

The billing software provider has fallen ~10% over the last few weeks, catching our eye ahead of their 1H results next week. The company has strong defensive qualities with their technology used in telecommunication and utility provider systems globally, historically seeing low levels of churn, strong cashflow generation and the ability to pass on inflation-linked price increases. They also have a solid M&A track record and a significant war chest to go after accretive acquisitions with such a strong balance sheet. Shares have been in no man’s land since BGH walked from takeover talks last year, however, the company has proven there are no skeletons in the closet and contract wins are coming through. We expect to see earnings grow from FY24 onwards, with near-term upside in M&A likely to prove the stock is cheap on just 18x PE multiple i.e. this is a profitable tech company, not one burning cash!

MM is bullish HSN ~$4.80, adding it to the Emerging Companies Portfolio Hit List

Add To Hit List