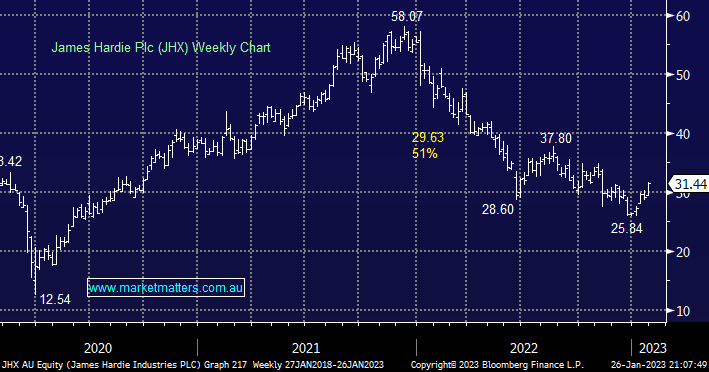

MM holds JHX in its Flagship Growth Portfolio and while it’s been a rocky road since our purchase in October we are showing a small paper profit at this point in time. The building materials business downgraded its FY23 guidance by around 7%, in October right after our purchase but following the initial dip the stock and sector appear to be slowly regaining their mojo, importantly we still believe JHX has the right strategy to drive margin recovery through FY23. As illustrated by DHI there’s no doubt that the US construction industry is slowing down but we’re conscious that JHX was trading around $58 only 12 months ago and “not too bad” is being received well in this battered sector i.e. there’s already plenty of bad news built into JHX’s share price

- We didn’t average JHX when it dipped in October due to the volatility of the stock (high beta) but we have remained positive its value ~$30.

MM is long and bullish JHX targeting the $37 area

Add To Hit List