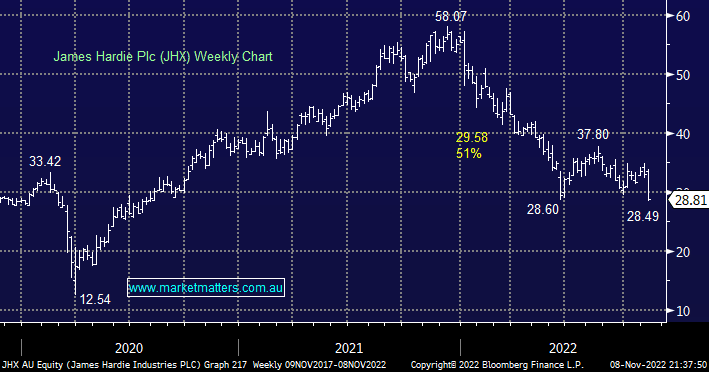

JHX was walloped -13.7% yesterday after the building materials business downgraded FY23 guidance, they are now expecting underlying earnings of $680m versus the market’s prior expectations of $730m, equating to a ~7% downgrade. Nobody ever likes/enjoys a downgrade to earnings but we feel it’s important to remember this is, not an operational issue simply the CEO being prudent towards the health of the housing market in North America, Europe and Australia i.e. people are building fewer houses which is understandable however it’s also important to note that 2/3rds of JHX earnings are linked to renovations, not new builds.

Housing is a cyclical industry and we all know its entered tough times as interest rates rise, we feel Aaron Erter whose only been at JHX for 2 months is being prudent with this downgrade, not an uncommon move when new executives take the helm and want to be in a position to “under promise and over deliver” come reporting season. However, we have no doubt that the US construction industry is slowing down but we should remain cognisant that JHX was trading around $58 only 12 months ago i.e. there’s already plenty of bad news built into JHX’s share price.

While guidance has reduced to US $650-710m, we still believe JHX has the right strategy and with input costs starting to moderate should drive margin recovery through FY23.

- We have been looking to increase our exposure to JHX below $29 i.e. “plan your trade and trade your plan”.

MM is bullish JHX from $29

Add To Hit List