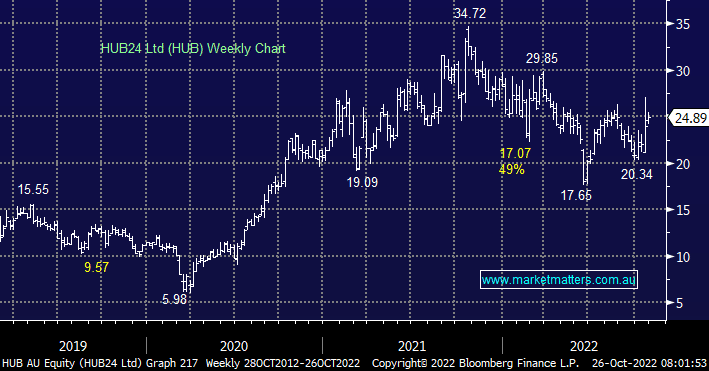

Independent platform provider HUB announced an excellent quarterly update last week which included net flows of $3.0bn and FUA of $68.4bn, taking it to the number one listed platform position for such net flows. HUB might not be a cheap play being priced as a growth stock but we believe it’s delivering on performance to justify its current valuation.

- HUB is winning more business than Netwealth (NWL) despite trading on an enterprise value that is ~60% lower i.e. it’s cheaper than its peers.

- we believe the outlook remains robust for HUB with advisors on the platform growing 4.4% quarter on quarter which when combined with 32 new distribution agreements lays the foundation for ongoing strong inflows.

MM is high conviction on HUB

Add To Hit List