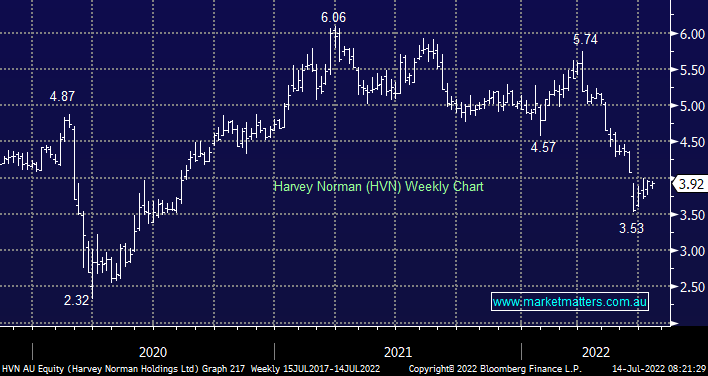

HVN is painting a very similar picture to the previous 3 stocks considered this morning, it again feels cheap trading on an Est. A valuation of 8.1x earnings for 2022 shows how negative the market has become on retail generally, and HVN specifically while its almost 9% yield has probably caught some yield hungry investors leaving them nurturing some paper losses.

- We believe HVN will turn when the whole sector regains its mojo but not before.

MM likes HVN into fresh lows under $3.50

Add To Hit List