Month: November 2015

Writing today’s report is one of the most difficult of recent times as we think about the people / families in Paris and the degree of guesswork it creates within markets.

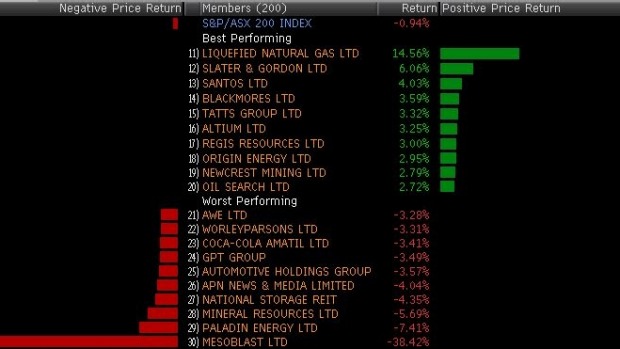

- Despite the ASX 200 ending its day 0.8% lower to 5,018, it was surprising for most to see it recover from the lows of 4,979 after falling below 5000 for the first time since September.

- BHP Billiton (BHP) recovered well from its lows, rallying 1.3% from $19.90 to end the day only 7c lower to $20.16.

- The big four banks were all off with Westpac falling 1.6 per cent, ANZ 1.5 per cent, CBA 1.3 per cent and NAB 1.4 per cent.

- Woolies dropped 1.8 percent and is trading at its lowest in over three years. Wesfarmers dropped 0.9 percent. We are watching these stocks as indicated in previous reports when we have called Woolies a sell.

- Telstra managed to buck the trend – around one in five stocks managed a gain – climbing 0.4 percent. Woodside climbed 1.3 percent as the energy sector enjoyed the day’s best gains as oil bounced in Asian trade. Santos added 4 percent, Oil Search 2.7 per cent and Origin 3 per cent.

- Gold miners also climbed, with Newcrest closing up 2.8 per cent.

- The day’s best was LNG Ltd, up 15 percent after the company announced the major construction contract pricing for its US LNG export venture, another step along the way of the regulatory approvals process.

- Mesoblast plunged close to 40 per cent following its disappointing float in New York’s Nasdaq exchange.

- In the gaming sector, Tabcorp (TAH) and Tatts Group (TTS) announced that they failed to agree on its possible merger agreement. This sent TTS to rally 3.1% higher to $4.04 while TAH ended 0.2% to lower $4.41.

- Talks resumed with Asciano (AIO) and Qube Logistics (QUB) as AIO granted QUB to conduct Due Diligence in its books.

Best Sector – Energy

Worst Sector – Industrials

Is the Resource sector simply too dangerous at the moment?

- Just a short afternoon note given the weekend report tomorrow.

- The ASX 200 performed in line with expectations and disappointed investors by ending the day 74 points lower (-1.5%) to 5,051 – Down 3.4% for the week! The market closed bang on the 5050 level we have spoken about in recent reports.

- As expected, BHP lost ground, down 1.8% to $20.23, however, it was surprisingly stronger than some of the Big 4 banks. It kicked extremely well from below $20 and will be watched extremely next week as indicated in the morning note.

- Commonwealth Bank (CBA) was the weakest link of the big four banks, shedding 2.1% to $75.76.

- The performance of specific stocks in the ASX200 this week is highlighted in the chart below, positive to see ANN one of our plays we own from higher levels having a good week.

- Please watch out for the weekend report where a close look will be taking at the current market.

Earlier in the week Market Matters made the aggressive call to switch Macquarie Group (MQG) into BHP Billiton (BHP), a stock that has fallen over 30% in the last year – see chart 1. A quick summary of the logic was that BHP looks technically in a support region from where it can bounce over $4 (~2%) and MQG had reached our target of fresh 2015 highs at the end of October – see chart 2.

- The ASX 200 recovered from an early sell-off and buyers returned at around 10.30am to push the market higher. After the unemployment numbers were released at 11.30am, the market continued to improve and at one stage was up 28 points. However, as the close approached, the sellers returned and the market closed up 3 points to 5,126.

- Santos (STO) returned to the bourse today after it raised $3.5b and the stock slumped by 27% hitting a low of $4.20. Volume today was over 59m shares, and it traded as high as $4.55 before succumbing to late selling and closed at $4.30. We will be covering STO more thoroughly in tomorrow’s morning note.

- Apparently the economy created 58,600 new jobs in October, well above the expected 15,000. This surge in employment has taken the jobless rate down to 5.9 per-cent, from 6.2 per-cent. This is the first time we have gone below 6 per cent since a one-off move in May this year. The jobs number put a rocket under the Australian dollar which surged up 1 per-cent to 71.28 US cents as investors start factoring in no more rate cuts. (see chart below – source Bloomberg)

- Dividend yields in the top 20 stocks are at their highest since the global financial crisis, but their recent share price performance suggests investor concerns are growing that these dividends may have to be cut. The average gross yield of the S&P/ASX 20 index, constituting companies that have been a staple of share portfolios for decades, is at 7 per-cent, the highest since 2008, according to data provided by Morningstar. (see chart below)

The broad-based market rout, which began in April has driven up yields, but the heavyweight banks and miners have been especially pummelled, losing a quarter or more of their share price value. - BHP had another rough day amid worries about the Brazil fallout. We will look to cover this in the a.m. note tomorrow.

It’s only a relatively short report today but an important one given the position of the market and what seems to be a nice aligning of our market expectations.

- In contrast to yesterday’s report, the ASX 200 managed to finish in positive territory today, but it felt like it was a hard slog to get there. The ASX 200 closed up 23 points to 5,122.

- China’s industrial output matched the weakest gain since the global credit crisis last month, while retail sales accelerated, underscoring a gradual shift in the economy towards greater reliance on consumer spending as old growth engines falter.

- The bad news: China began the fourth quarter with little change in momentum from the end of the previous one, signalling that monetary and fiscal easing have yet to spur an acceleration in growth. Goldman Sachs analysts are among those that predict the central bank will take further actions as a result. Industrial output rose 5.6 per cent in October from a year earlier, matching January through March’s reading which was the weakest since 2008. Fixed-asset investment increased 10.2 per cent in the first 10 months – the slowest pace since 2000 – while retail sales climbed 11 per cent in October, the quickest gain this year.

- The resources were a drag on the market, with BHP Billiton (BHP) down 62c (-2.9%) to $20.95 after hitting a low of $20.88. RIO Tinto (RIO) tried hard to remain positive and edged 1c higher to $49.40. BHP, the world’s largest miner, saw its shares fall to their lowest intraday level since 2008 after a dam burst at a mine it partly owns, resulting in at least six deaths and dozens more missing. We did emphasise that BHP is a volatile investment but are still predicting a bounce over the short term.

- It was reported today that TPG Telecom (TPM) are going to the market to raise $300 million through an institutional placement. It is expected that the funds will be used to pay down debts associated with its purchase of iiNet in July this year. TPM were in a trading halt today.

- Fortescue Metals (FMG) reported today that it was repaying US$750m ($1.07b) in an effort to reduce interest costs. FMG closed 3% higher at $2.37.

- ANZ shares enjoyed a rare break from the recent gloom surrounding bank stocks, rising by 2.9 per cent to $26.29, the biggest increase of the big four today.The increase comes hot on the heels of a change in view from, UBS. We at Market Matters think ANZ has got to a point where it is heavily oversold.

Best Sector – Energy

Worst Sector – Materials

Winners

Qube Holdings Ltd (QUB) +$0.13, or (+6.0%) to $2.31

Regis Resources Ltd (RRL) +$0.115, or (+5.9%) to $2.05

Mayne Pharma Group Ltd (MYX) +$0.05, or (+4.7%) to $1.11

APN News & Media Ltd (APN) +$0.02, or (+4.0%) to $0.515

When the US starts raising rates what usually happens?

- The ASX 200 finished down 20 points at 5,099, and it feels like we had a good day! At its worst the index was down 85 points, but from ~2.30pm the buyers started in and the market looked a whole lot better. The market bounced off our ABC target recently referenced in the reports of 5050.

- The resource sector held the very well with BHP Billiton (BHP) finished up 15c to $21.57, whilst RIO Tinto (RIO) was positive for 90% of the day, finishing up 39c to $49.39.

- The worst sector today seen was in the IT sector, with Computershare (CPU) shedding 23c (-2.1%) to $10.58 and IRESS (IRE) down 26c (-2.8%) to $9.16.

- As mentioned this morning, AIO was in the middle of a ‘bidding war’ between QUB and Brookfield. AIO rallied 3% to $8.99.

- Qantas (QAN) continues to lose its lustre, down 1.4% to $3.66, despite Crude Oil plummeting lately. The weakness is thought to be due to the prospect of US interest rates rising in the near term, where their funding is offshore.

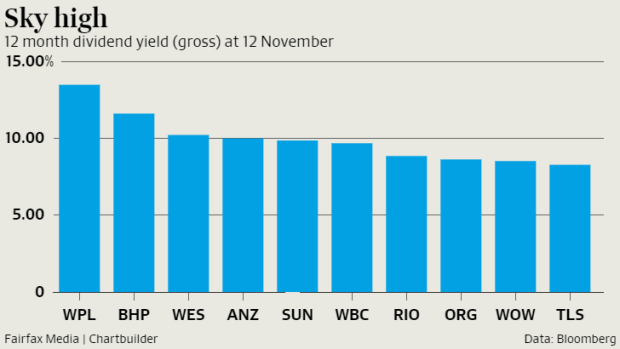

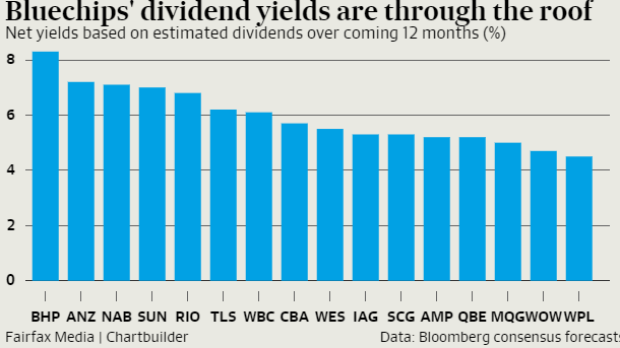

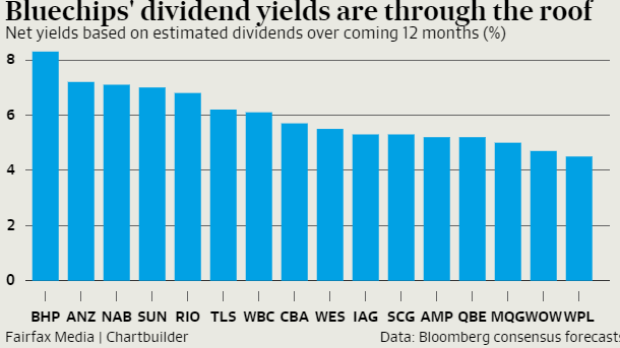

- The chart below (source www.smh.com.au) shows dividends of some of the ASX’s biggest names. BHP promises a net yield of 8.3 per cent, while other names like ANZ, NAB and Suncorp are trading on yields of around 7%. Once franking is added it’s closer to 10%. The question moving forward is how sustainable are these? Market Matters has bought BHP for a bounce, own ANZ for yield and a small amount of growth, like SUN technically and fundamentally, but are the least confident in NAB moving forward. It will be interesting to watch the performance of these stocks over the next 12 months.

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.