Month: August 2015

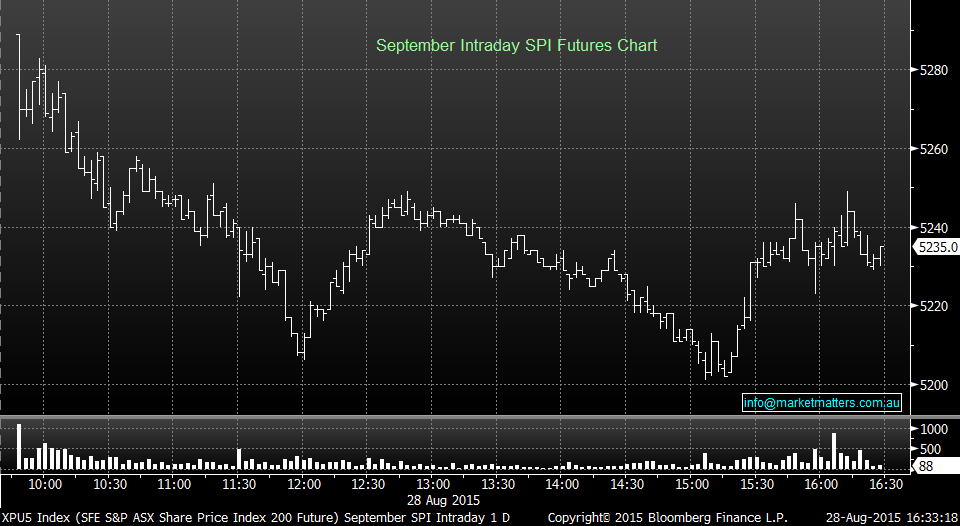

- The ASX 200 succumb to an earlier report, that the Chinese Government announced they would not step into the market if there was continued selling. The ASX 200 finished the day down 56 points (-1.1%) to 5,207.

- The worst sector was Consumer Staples – Woolworths (WOW) ending its day down $1.00 (-3.7%) to $26.40, Wesfarmers (WES) was also weak, down $0.79 (-1.9%) to $40.66, whilst Metcash (MTS) fell a similar amount, down $0.02 (-1.8%) to $1.085.

- Not even the oil or metal stocks were able to finish in the black, given the stronger prices over the weekend. BHP Billiton (BHP) finished $0.31 (-1.2%) lower to $25.18, RIO Tinto (RIO) fell $0.81 (-1.6%) to $50.29, whilst Fortescue Metals (FMG) managed to finish up 1c to $1.91.

- The ‘winners circle’ included Flight Centre (FLT) that continued a strong week last week, up $0.61 (+1.7%) to $37.01 and Cochlear (COH), up $0.35 (+0.4%) to $85.43. In the banks, Bendigo Bank (BEN) finished up after being sold off last week, up $0.15 (1.4%) to $10.97.

Best Sector – Industrials

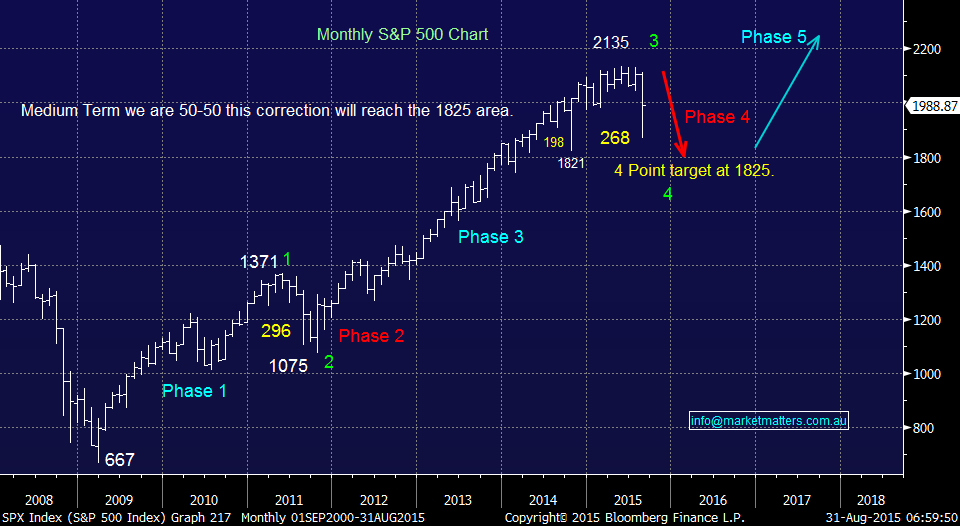

We all know that last week brought extreme volatility to the markets but not necessarily total panic. This is evidenced by the fact that investors did not flock to gold as one might normally expect and treasury yields closed higher than the previous week. Hence, we feel most experienced investors, like ourselves, simply saw last week as a great buying opportunity of discounted equities. For example, the S&P500 illustrated on chart 1 hardly took a back step in its advance since late 2011

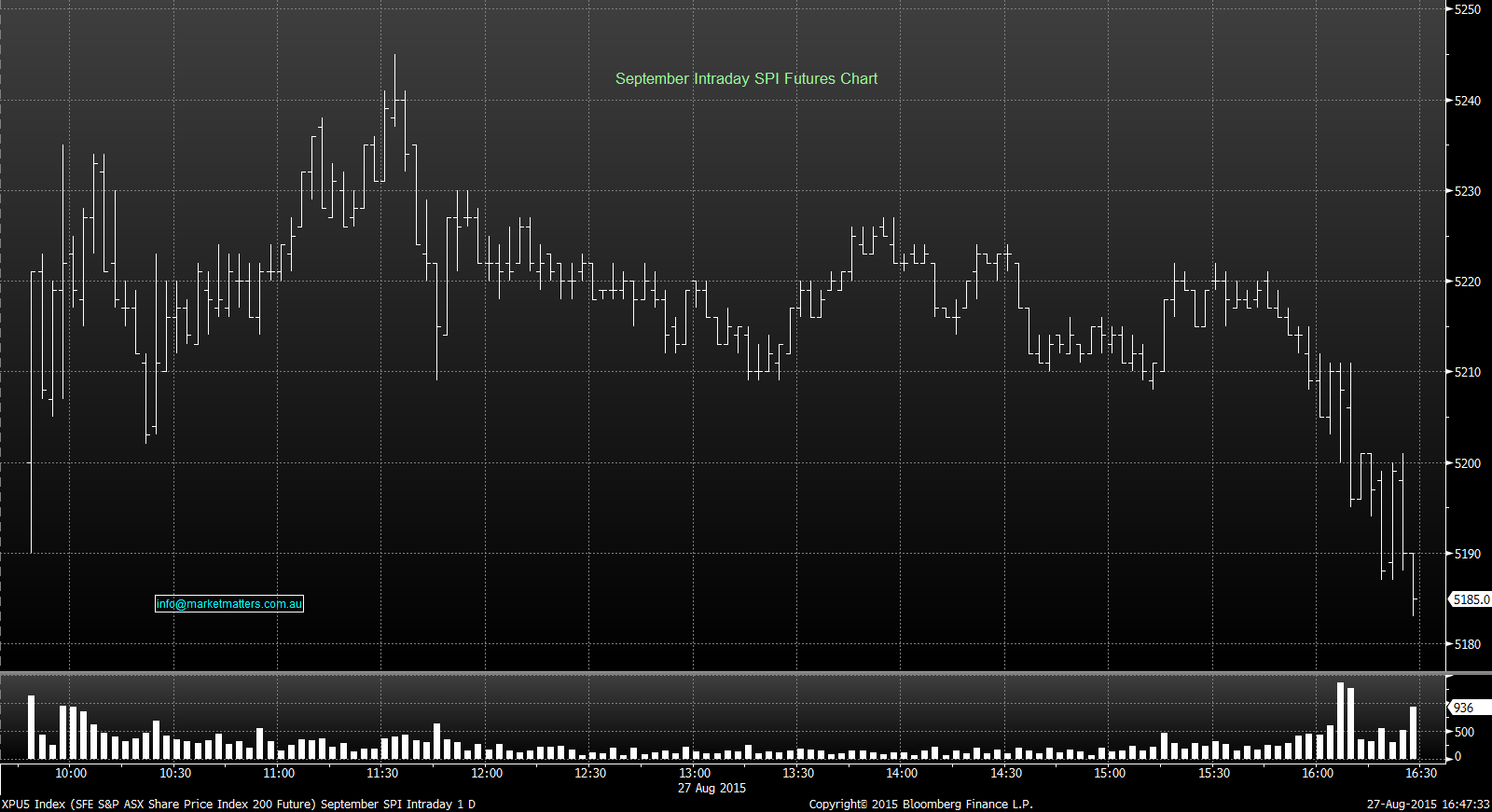

- A choppy session was experienced yet again in the ASX 200, ending unchanged for the day.

- The ‘yield stocks’ looking tired, with Commonwealth Bank down 7c at $76.36 and Telstra (TLS) down 8c at $5.82.

- The Resource sector was the shining star today, BHP rallied 5.9% at $25.49 and RIO up 4.7% at $51.10 as the China Government continues its support in its market.

- Watch out for the Weekend Report…

Best Sector – Materials

Worst Sector – Telcos

It’s always refreshing to our views on the market be supported by market action. So, as we turn on our screens and the Dow is up another 369 points (2.27%) is the panic over China finished so that equities will refocus on fundamentals closer to home? Certainly the extreme volatility of the last week will settle but there is no doubt that the market will be nervous for a while yet.

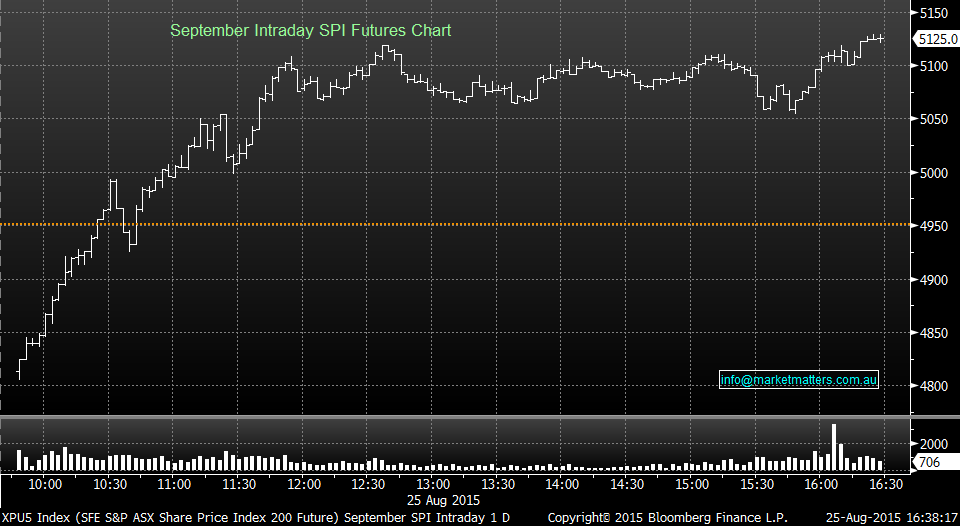

- A positive, but choppy session today in the ASX 200, trading as high as 5269 by mid-day, before fading back to close 60 points higher (+1.2%) at 5,233.

- The Banking Sector continued to drive the broader market higher – ANZ was the strongest link rallying 1.8% at $28.57.

- Reporting Season continues .

- Nine Entertainment (NEC) closed 3.5% higher at $1.50 as investors welcomed their full year 2015 results, despite reporting at 2.9% lower from previous year.

- Ramsay Health Care (RHC) closed 5.5% higher at $63.68after reporting a net profit rise of 27%.

- Billabong (BBG) closed 2.4% higher at $0.645 as investors see a recovery in the company.

- Flight Centre (FLT) soared 11.5% after forecasting a solid earnings for the year ahead.

- Volatility eased off today, however, we still expect a choppy few sessions.

Best Sector – Utilities

Worst Sector – Materials

The volatility in the markets continues to dominate headlines and investor uncertainty. Essentially markets were over extended on the upside so that as the ‘spring’ was stretched further so the reaction would be more volatile. This has been mentioned in our analysis of the VIX and its extended period of low volatility. In our view and consistent with our market themes, the extreme market gyrations experienced this week provide opportunity for investors and traders.

- Another choppy and volatile session today in the ASX200, opening near its lows, only to be able to push a little and tread above water by the afternoon. The ASX 200 finished 35 points higher (+0.7%) at 5,172.

- The Banking Sector resumed its slow recovery, with Commonwealth Bank (CBA) up $1.05 (1.4%) to $76.13 and Westpac (WBC) up $0.38 (+1.2%) to $31.28.

- The Resource sector had a great day, BHP closed 2.6% higher at $23.94, while its spin-off, South32 (S32) managed to lose 3.9% at $1.47

- Woodside Petroleum (WPL) roared 2.6%, despite trading ex-dividend (89.61c fully franked). We currently hold WPL.

Best Sector – Energy

Yesterday was an amazing day that saw the ASX200 rally well over 4% intra-day to close up a very healthy 136 points (+2.7%). In simple terms the value that returned to the market was too good to resist and investors aggressively chased value, especially in the banking sector which closed up 4% after opening well in the red e.g. ANZ rallied 6% to close at $27.99 after opening at $26.41 – see chart 1. When panic hits a market its time to simply to stand back and keep it simple stupid (KISS).

- The Sentiment has finally turned… for now. The ASX200 rallied 209 (+4.2%) from its session low of 4928 and finished at a pleasant level of 5,137.

- China however, continued its landslide, the Shanghai Composite Index is currently down 6.4% to 3,005 as we type.

- The Banking sector led the way back from the deep end, as Westpac (WBC) recovered 4.9% and closed at $30.90, while Commonwealth Bank (CBA) ended 3.6% higher to $75.05.

- The consumer sector too, roared, with Woolworths (WOW) up 5.3% to $26.62 and Metcash (MTS) up 3.4% to $1.08.

Best Sector – Financials

Worst Sector – Telcos (TLS ex-dividend today)

Our Investing Journey Together, Clearly got Tougher, but also VERY Exciting!We started writing this report before 6am this morning, after basically no sleep, courtesy of an amazing night in the markets. The Dow closed down 588 points, BUT over 500 points above its intra day lows – yes the Dow was down over 1000 points at one stage last night! Clearly the news is full of all the reasons why equity markets are “collapsing”, but often context is forgotten for a good story. The Dow had rallied for over 3 years without a 10% correction, that is statistically extremely unusual, as opposed to what we are experiencing now, which is actually common, just more dramatic than usual. Very importantly, we believe this is a sharp correction within a bull market, NOT the start of a bear market – similar but more dramatic to what we experienced in 2011. We believe the market is simply punishing investors who were greedy / too optimistic and forgot that markets move in cycles and the odds were clearly in favour of this current corrective move.

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.