Month: July 2015

The gold price and major related stocks have traded in an uncanny fashion lately, exactly as we have been forecasting. This happened at the end of 2014 enabling us to enjoy significant gains from both Regis Resources (RRL) and Newcrest Mining (NCM), hence our excitement as markets unfold again. – Remember we won a “steak at Rockpool” from a trader on Livewire by forecasting that NCM would outperform CBA from December 2014 until March 2015 – https://www.livewiremarkets.com/ . Generally gold stocks pay little or no dividend, hence when purchasing, timing is vital to potentially achieve capital gain.

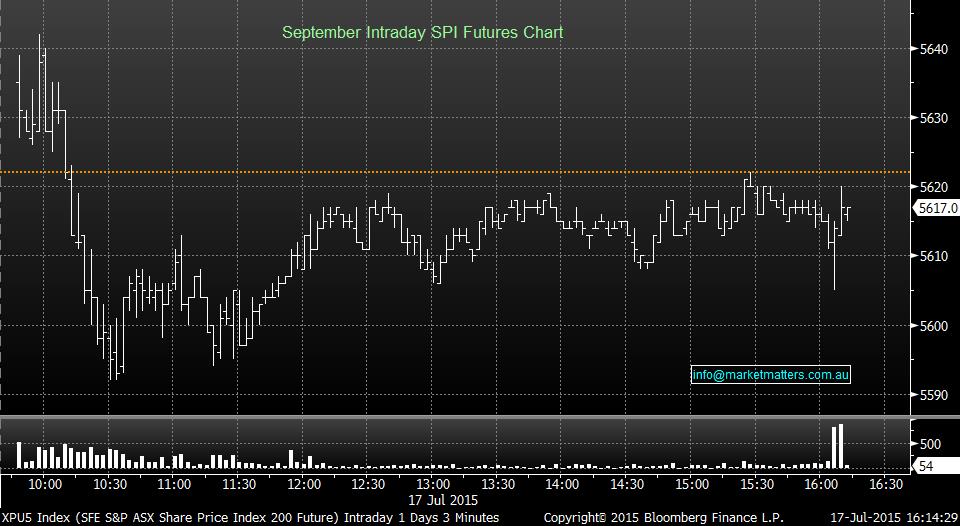

• It was a dull and choppy session in the ASX200 today, ending only 2 points higher at 5,671.

• Much of the action was witnessed in the first hour of today, trading as high as 5,689 to a low of 5,647.

• Macquarie Group (MQG) continues to dominate the Financials Sector, up 0.5% at $83.51, ending the week up 3.6% as investors see positive earnings in the US financials.

• The Gold sector had a great day (see this morning’s report), with Regis Resources (RRL) roaring 26% higher at $1.45 and Newcrest Mining (NCM) up 1.4% at $13.20. Subscribers would have received a live alert when we entered into the gold trade today.

• In the telco sector, Vocus (VOC) conquered the sector and closed 2.5% higher at $5.70.

• Watch out for the weekend report.

*Greek Parliament votes in favour of bailout plan – no great surprise.

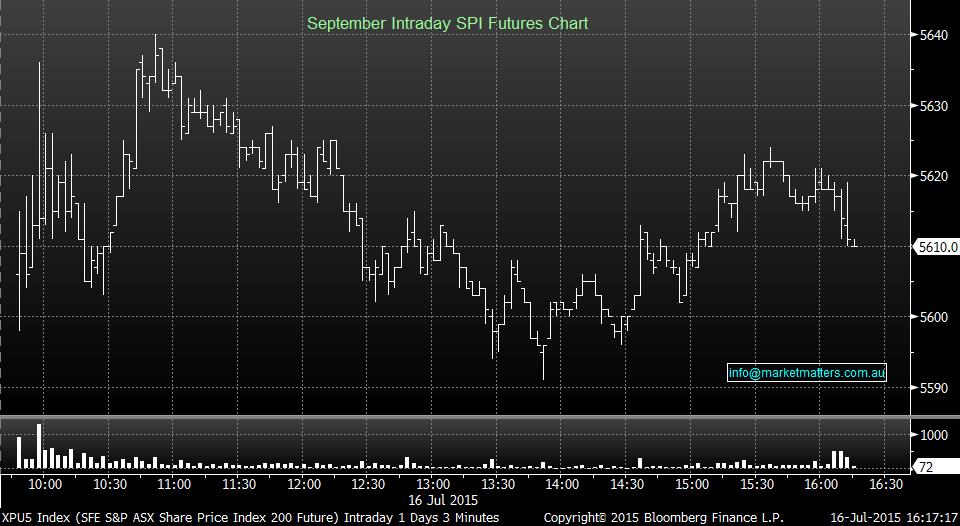

• A choppy session was witnessed today in the ASX 200, ending 33 points higher (+0.6%) at 5,669 with a range of 47 points.

• With our Resource rich brethren, Canada reducing its interest rate to 0.5% overnight, there would be no surprise if we saw global investors switching from Canada into Australia with a current interest rate of 2%.

• The Banking sector again did the heavy lifting – National Australia Bank (NAB) rallied 1.6% at $34.32 and Westpac (WBC) up 1.9% at $34.63.

• QBE Insurance rose 2% at $14.67 after investors welcomed their announcement of selling its North American mortgage and lending business for ~$90m.

This week we have witnessed Facebook (FB.US) become a $US250bn company. The fastest company to reach this milestone, amazingly now larger than BHP, CBA and Woolworths (WOW) combined. Mark Zuckerberg’s social network company, as illustrated in the movie “The Social Network”, was born only 11 years ago in a Harvard student room. Facebook has achieved so much in just over 10 years compared to what the 3 iconic Australian companies have in recent decades. This is a clear lesson for investors to move with the times, a great company for investors last decade, is not necessarily a great company for the next decade. One exciting aspect of the booming IT industry is the ease / cost of entry, for example no large deposit of Iron Ore is required – come on Australia, time to catch up on the innovation! Today we have focused on 4 pioneering IT companies in the US to identify the short term direction of the broader index.

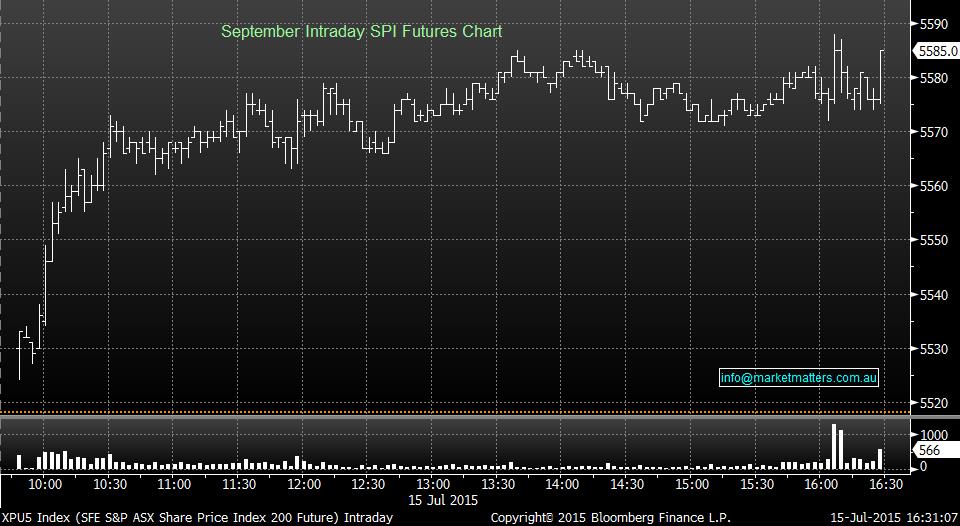

• The ASX200 rallied 59 points (+1.1%) at 5,636, closing on its highest level in over 6 weeks.

• The banking sector contributed to ~20% of the broader market’s gain, with Commonwealth Bank (CBA) ending the day 1% higher at $87.12 and Westpac (WBC) up 1% at $34.00.

• Resources mining giant, BHP Billiton (BHP) lost 0.7% at $26.90 after announcing an impairment charge of ~US$2bn on one of its gas project. The write off as not a surprise, however it was announced earlier than anticipated.

• Telco, Amaysim (AYS) debuted with a slow start, only to rally towards the last hour of the session and end 5.6% higher from its IPO price of $1.80 to $1.90.

• Diversified Financials, Perpetual (PPT) lost 6.6% at $45.60 after announcing it had lost ~$1.6b of fund outflows in the last 3 months ending June 2015, with market conditions being the culprit.

The US Looks Good For Now, but The ASX200 Has Headwinds

• The ASX200 played catch up today, rallying 104 points (+1.9%) and catching up on the global equity markets’ performance overnight.

• It was a pleasant day not witnessing a sea of red today, with the materials sector being the strongest link. BHP Billiton (BHP) closed 2.6% higher at $27.10 while Fortescue Metals (FMG) rallied 3.8% higher at $1.79. We currently hold FMG via call options as a TRADE ONLY.

• China remains to be in a volatile position, with the Shanghai Composite currently trading 1.2% lower at 3,924 and the China A-Listed stocks down 3.6% at 4,000.

• The overseas Indices are currently looking to take a breather and consolidate tonight, with the likelihood of losing some of yesterday’s gains.

How does the Insurance Sector look after Warren Buffet’s foray into IAG?

• The ASX200 repeated much of last Friday’s session, trading near its lows early in the session, as low as 5,451, only to rally by lunch as high as 5,543 and drift back below the red sea by 19 points at 5,473. It seems that risk will remain off the table until Greece responds to the Eurogroup’s demands no later than Wednesday.

• As expected, volatility remains and the trading range of the ASX 200 were close to 100. The banking sector led the choppy session today, as Commonwealth Bank (CBA) closed 61c lower at $85.18 after trading as low as $85.00 and as high as $86.83 today.

• Although Iron Ore is currently trading slightly higher in Asia, Fortescue (FMG) lost 5% at $1.725 and South32 (S32) down 4.2% at $1.705.

• China also contributed in today’s session, reporting its trade balance at US$46.54B, ~18% lower than analysts’ expectations. The China A-share index resumed its rally however, with ~26% of its ~1300 stocks on trading halt resuming trade today. The China A-Share futures index are currently trading 2.2% higher this afternoon and with the Peoples’ Bank of China (PBoC) providing liquidity to stabilise the market, a restore is in order and the market is ok for now.

Really bullish, there's more to go in the reflation rally

Please enter your login details

Forgot password? Request a One Time Password or reset your password

One Time Password

Check your email for an email from [email protected]

Subject: Your OTP for Account Access

This email will have a code you can use as your One Time Password for instant access

To reset your password, enter your email address

A link to create a new password will be sent to the email address you have registered to your account.

Enter and confirm your new password

Congratulations your password has been reset

Sorry, but your key is expired.

Sorry, but your key is invalid.

Something go wrong.

Only available to Market Matters members

Hi, this is only available to members. Join today and access the latest views on the latest developments from a professional money manager.

Smart Phone App

Our Smart Phone App will give you access to much of our content and notifications. Download for free today.