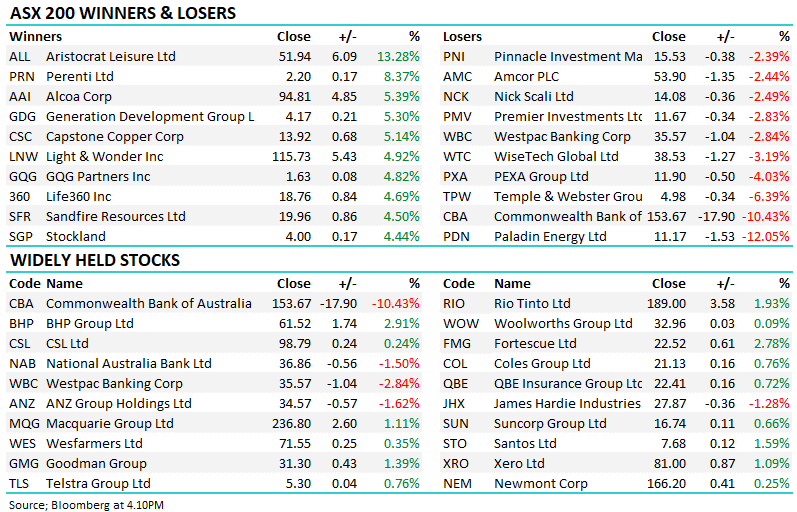

Multi-affiliate investment group PNI has been a stellar performer since late 2023, with the share price more than doubling. The market embraced its recent AGM, reinforcing a strong FY24, during which it reported a 7.6% lift in revenue and an 18% jump in profit, with some brokers upgrading their price targets above $21. We will don a slight contrarian hat here, believing that while we wouldn’t call it a sell, it is feeling “as good as it gets” short-term, i.e. we like the idea of buying a dip but wouldn’t chase current strength. This stance is supported on the valuation front with the stock rich compared to history as it already builds in plenty of good news over the coming years.

- We like PNI closer to $16, a move that will probably need a significant market pullback to be achieved.

MM is neutral toward PNI

Add To Hit List