The ASX 200 ended the week up +1.4 %, taking the month’s gains to +2.7%, as the index pushed within striking distance of February’s all-time high. The energy and tech sectors drove the gains, both ending the week by more than 5%, while defensive/rate-sensitive stocks dragged the chain, i.e. “risk on” was the order of the day. Out of the mainboard’s 11 sectors, only the consumer staples, Utilities, and real estate sectors closed lower. The US-China “Trade Truce” set the platform for a strong start to the week, before the Australian market posted its highest level in three months on Friday after soft US economic data paved the way for interest rate cuts in Australia and the United States. The positive statistics are continuing to line up:

- The ASX200 has rallied for eight consecutive sessions, its longest winning streak since August, with the index closing higher in three out of the last 4 weeks

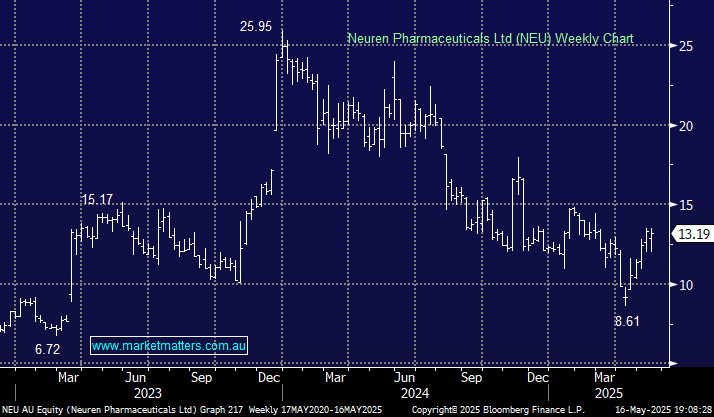

The winners and losers over the week were a fairly eclectic bunch, although the gold stocks and defensives did dominate the wrong side:

Winners: Life360 (360) +27.6%, Block (XYZ) +12.4%, HMC Capital (HMC) +10%, Pro Medicus (PME) +8.9%, Megaport (MP1) +8.6%, Whitehaven Coal (WHC) +7.8%, Lovisa (LOV) +7.6%, Woodside (WDS) +7.5%, Flight Centre (FLT) +6.6%, IPH Ltd (IPH) +6%, and Sandfire (SFR) +4.7%.

Losers: Insignia (IFL) -13.4%, Evolution (EVN) -8.8%, Eagers (APE) -8.5%, Regius Resources (RRL) -8.3%, Deep Yellow (DYL) -7.4%, Newmont (NEM) -7.3%, Aristocrat (ALL) -5.8%, AGL Energy (AGL) -5.3%, Dexus (DXS) -4.9%, and NRW Holdings (NWH) -3.5%

Things again steadily improved on the tariff front at the start of the week after the truce with China fuelled the risk-on tone that drove the US stock benchmark to the brink of a bull market, surging almost 20% from its April low as fears of a bad tariff outcome faded rapidly:

- This week the RBA meets, with a 0.25% rate cut expected on Tuesday, but the accompanying rhetoric is likely to garner the most attention.

- Last week’s local unemployment data was stronger than expected, supporting a potentially less dovish easing approach by the RBA.

- However, the market is a fickle beast, and after some softer economic data from the US, rate cut hopes remained entrenched – credit markets are pricing in a 99% chance of a rate cut on Tuesday.

- Stocks and Trump will have a couple of hurdles to clear this week, with Moody’s downgrading US debt on Friday and his initial attempt to get his massive tax cut bill passed has failed.

We continue to believe the ASX200 and other major global indices will follow the German DAX and post fresh all-time highs in 2025 with a “risk on” bias likely into Christmas:

- We anticipate that the ASX will rally through 2025 with its all-time high now only 3.3% away: what tariffs!

Overseas markets were solid on Friday night, with US stocks registering their second-best week of 2025. In Europe, the EURO STOXX 50 gained 0.3% while the UK FTSE doubled these gains to close up +0.6%. In the US, the S&P 500 closed up +0.7%, with the index climbing over 5% for the week. Fund managers added around $US20 billion to American stock funds in the past week, the first inflow to the region in over a month.

- The SPI Futures are calling the ASX 200 to open marginally lower on Monday, with weakness in the resources likely to weigh on the index.