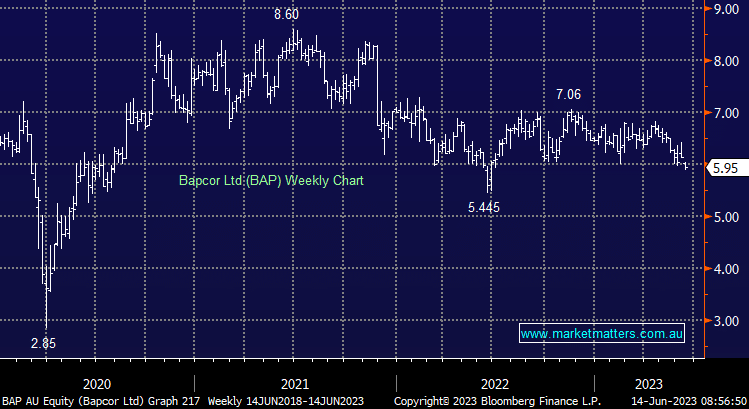

The auto parts company closed below $6/share for the first time in nearly 12 months following Citi downgrading the stock to a hold from a buy on two main concerns. The first is a slowdown in retail spending impacting near-term earnings. Citi references Super Retail’s recent trading update as a sign consumers have pulled back discretionary spending, however, the update in May showed that their Auto brand was growing at 5% on a LFL basis. Hence, while retail concerns are valid, it appears any spend on aftermarket auto products seems to remain resilient, which holds true historically as well.

The analyst also flags a potential slowdown in the Thailand growth story which would be likely to weigh on medium-term earnings. Bapcor has been focussed on the Better than Before plan which aims to increase margins and add $100m to EBIT by FY25. We don’t see this as being priced in, and we are backing management to make some early inroads, picking the low-hanging fruit this half which supports a beat at the FY results in a few months. While this focus may delay the international ramp-up story, we would prefer the company to get their main earnings drivers in order first before splashing the cash to aggressively expand into Thailand.

MM is bullish BAP but has the position on a tight leash

Add To Hit List