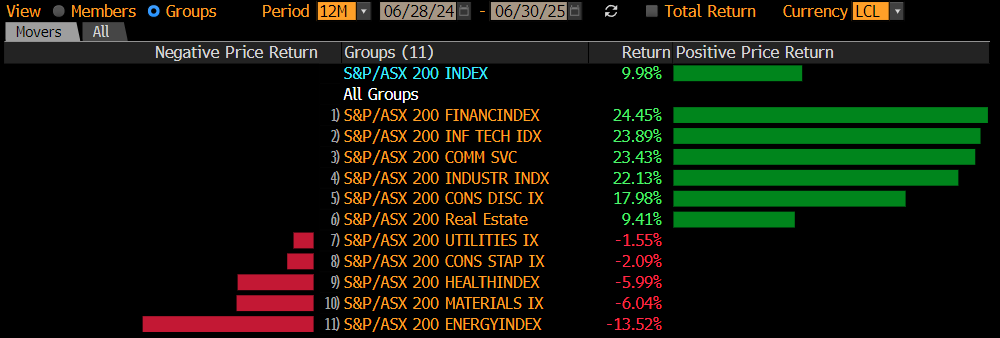

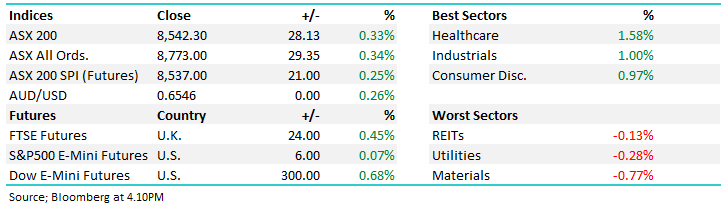

The ASX200 finished the week up just +0.1% after Friday’s sharp, almost 100-point reversal lower from early highs, led by the banks, taking the index back towards the 8500 level. However, under the hood, not everyone danced as one, with eight of the mainboards’ eleven sectors retreating, led by energy and utilities, while the advances by the heavyweight financial and resources were enough to ensure the index closed positive, albeit just:

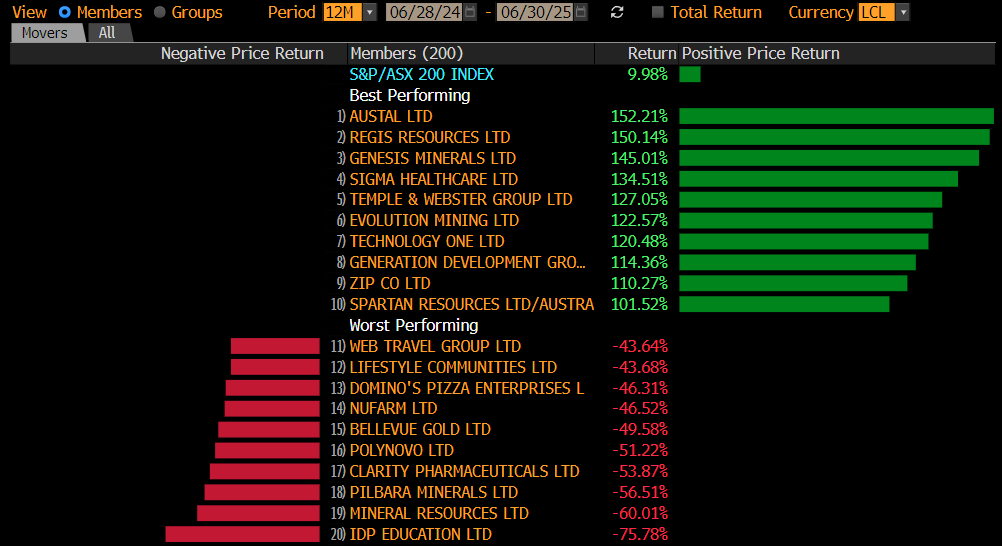

By the end of the week, the winners and losers enclosure contained an eclectic bunch as we head into the EOFY, although again, the gold stocks came under significant pressure. At the same time, copper names returned to the winners’ enclosure. Also, note that when evaluating your portfolios over the week, several stocks traded ex-dividend, especially in the real estate and utility sectors:

Winners: Clarity Pharma (CU6) +21.2%, Light & Wonder (LNW) +13.4%, Capstone Copper (CSC) +12%, Pilbara (PLS) +11.8%, Paladin Energy (PDN) +8.8%, HUB24 (HUB) +6.1%, Metcash (MTS) +5.7%, Macquarie Group (MQG) +5.4%, and ANZ Group (ANZ) +2.9%.

Losers: Emerald Resources (EMR) -16.2%, Reece (REH) -12.8%, Northern Star (NST) -10.7%, DigiCo (DGT) -9.3%, Woodside Energy (WDS) -8.2%, Fletcher Building (FBU) -7.9%, Sigma Health (SIG) -6.1%, Guzman & Gomez (GYG) -5.9%, Xero (XRO) -5.6%, and Brambles (BXB) -4.8%.

On the economic and geopolitical front, the markets’ focus has moved on from tariffs and the Middle East to Jerome Powell and the Fed, at least for now:

- On Monday, markets were confronted by the news that the US had bombed nuclear facilities in Iran, but after an initial downside reaction, the bulls again took control.

- On Tuesday, Jerome Powell’s balanced comments about inflation and rate cuts were taken positively by traders, who priced in at least two rate cuts in the US by Christmas.

- The massive $1.85bn capital raise by Xero (XRO) sapped some buying liquidity from the market before June 30th, but the impact was minimal, with many investors caught underweight equities it seems.

- On Wednesday, the Australian monthly CPI inflation print was softer than expected, reaffirming market bets for an RBA cut in July; futures markets are 94% certain.

- Later in the week, no bad news was enough to see the US S&P 500 pop to fresh all-time highs.

Overseas markets ended the week with a bang as the S&P 500 advanced +0.5% to an all-time high, as traders dodged a flurry of tariff headlines to drive stocks higher, capping a week that saw a cooling in Middle East tensions and signs the US economy is holding up amid subdued inflation. European stocks also enjoyed a positive Friday after US indices posted their first new high since February, the EURO STOXX 50 surged +1.6%, and the French CAC +1.8%.

- The SPI Futures are calling the ASX200 to open marginally higher on Monday following the strong session on Wall Street.