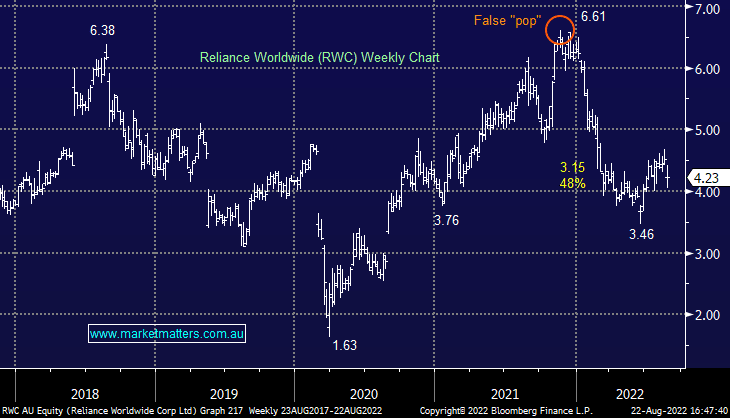

RWC -6.21%: The supplier of plumbing parts was down as much as 10% at its worst today on a result that looked at least in line with expectations. Net sales of $US1.17bn were online with consensus while adjusted net profit of $137.4m was 2% lower than FY21 but in line with the $138m expected. They said that while the short-term outlook is “satisfactory” the medium-term outlook is uncertain, although we think that RWC’s focus on repairs should position better than others through any downturn. One obvious risk is the destocking from wholesalers who bought up big at the end of FY22 due to supply chain issues and that should have a negative impact at the start of FY23. They also talked to higher commodity costs for key materials including copper, zinc, resins, and steel, along with freight, packaging, energy and other cost inflation. They said average price increases across the group of about 9.5% were achieved during the period, with price rises implemented in all key markets helping to offset cost increases. That has been an obvious theme through this reporting season where consumers have (so far) handled higher prices.

MM is neutral RWC ~$4.20

Add To Hit List