- Markets @ Midday: Listen here at lunchtime or find all Market Matters Podcasts on Spotify.

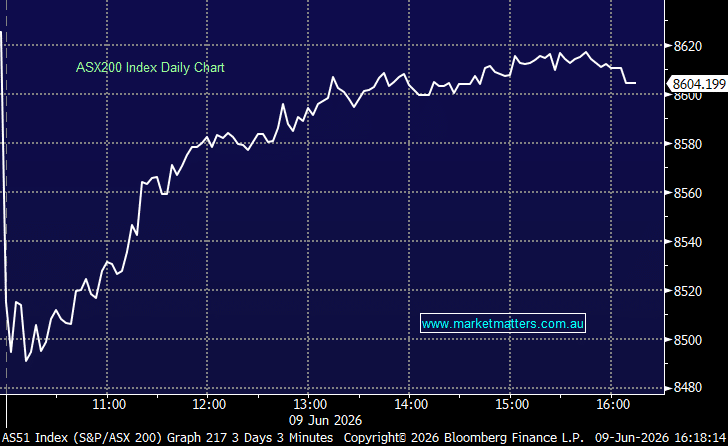

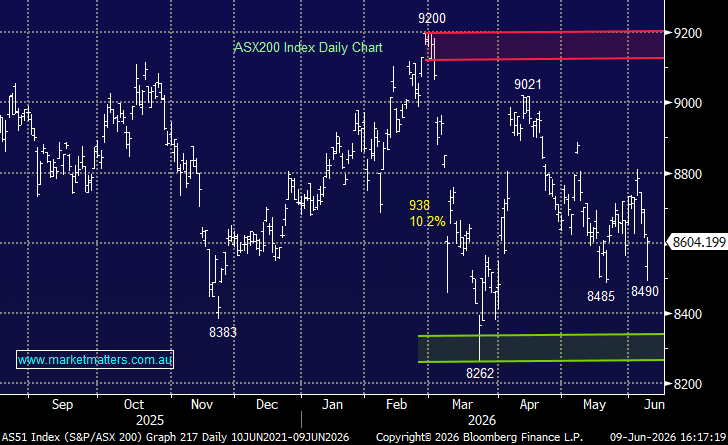

The ASX spent most of today digging itself out of an early hole, with the market initially rattled by implications of Friday night’s strong US payrolls report before steadily recovering through the session. After falling sharply at the open, buyers gradually returned and by the close the index had trimmed the bulk of its losses – the market remains willing to buy weakness despite ongoing uncertainty around rates.

Materials and gold stocks remained under pressure as higher US rate expectations weighed on commodities, while Technology also struggled following weakness in the US on Friday night. On the flip side, investors rotated back into defensives, with supermarkets, healthcare and parts of the banking sector finding support as the market digested NAB’s view that the next RBA move is now more likely to be down than up.

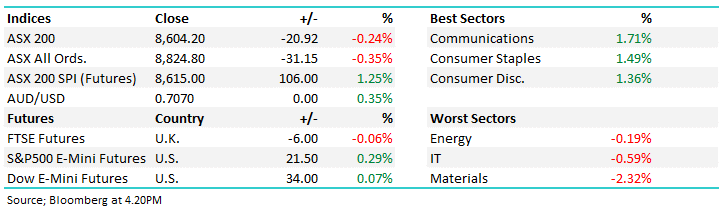

- ASX 200: 8,604.20 / −20.92pts / −0.24%

- AUD/USD: 0.7070 / +0.35%

- Best sectors: Communications +1.71%, Consumer Staples +1.49%, Consumer Disc. +1.36%

- Worst sectors: Energy −0.19%, IT −0.59%, Materials −2.32%

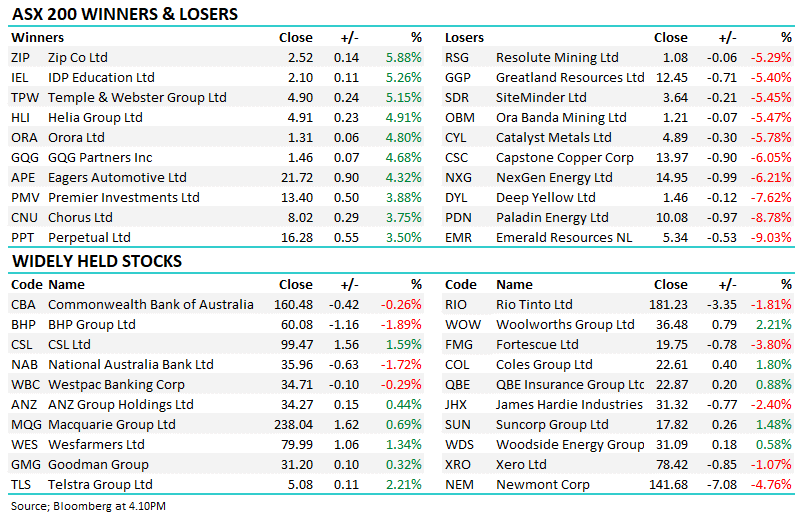

- oOh!media (ASX: OML) +9.56% to $1.37 surged after receiving a $765m takeover proposal from Bain Capital, setting up a potential bidding battle with Pacific Equity Partners and I Squared Capital.

- Gold stocks were under pressure as higher US rate expectations weighed on bullion, with Newmont (ASX: NEM) −4.76% to $141.68 and Northern Star (ASX: NST) −3.32% to $19.22 among those lower.

- The major miners struggled, with BHP (ASX: BHP) −1.89% to $60.08, Fortescue (ASX: FMG) −3.80% to $19.75 and Rio Tinto (ASX: RIO) −1.81% to $181.23 weaker as iron ore hovered near US$100/t and copper prices eased.

- Technology names recovered from steeper early losses but still finished lower, with WiseTech Global (ASX: WTC) −4.55% to $38.00 and Xero (ASX: XRO) -1.07% to $78.42 dragged down by the broader AI-related selloff. Megaport (MP1) +3.03% to $19.04 bucked the trend following on from their blockbuster capital raise last week.

- Investors rotated into defensives, with Coles (ASX: COL) +1.80% to $22.61 and Woolworths (ASX: WOW) +2.21% to $36.48 both extending recent gains as uncertainty around growth and rates persisted.

- Healthcare also found buyers, with Cochlear (ASX: COH) +2.18% to $102.64 and CSL (ASX: CSL) +1.59% to $99.47 outperforming.

- James Hardie (ASX: JHX) −2.40% to $31.32 said it would vigorously defend a shareholder class action alleging the company misled investors over earnings forecasts.

- Coast Entertainment (ASX: CEH) +10.71% to 46.5c jumped after moving closer to a final decision on its proposed Dreamworld precinct development, following a positive planning response from Queensland authorities.

- Bapcor (ASX: BAP) +4.76% to 44c edged higher after appointing former Bank of Queensland chairman Andrew Fraser to its board from July.

- Qube Holdings (ASX: QUB) +0.40% to $5.02 gained after Papua New Guinea’s competition regulator backed Macquarie’s planned $11.7bn takeover, clearing another key hurdle for the deal.

- Atlas Arteria (ASX: ALX) +0.20% to $5.08 remained in focus after highlighting the limited support received so far for IFM Investors’ $4.75 per share takeover proposal, with the board reiterating that the offer materially undervalues the business.

- Oil (WTI): ~US$89.80/bbl / -1.6%

- Gold: ~US$4,343/oz / +0.3%

- Iron Ore: ~US$100.80/mt / +0.8%

- Asian Markets: China +1%, Hong Kong +0.21%, Nikkei +2.04%

- Global Futures: FTSE Futures: −0.3% / S&P 500 E-Mini: +0.29% / Dow E-Mini: +0.07%